Four quality companies at record-low valuations

The market is handing investors a gift right now. Most are too scared to take it.

AI disruption fears have hammered some of the best software businesses on earth. Not struggling companies. Not overpriced growth stories. Companies with decade-long track records of generating exceptional returns on invested capital, now trading at their cheapest multiples in years.

This is what behavioral economics calls the availability heuristic. Recent events (AI replacing software) feel more probable than the base rate suggests. The market is pricing in disruption that hasn’t materialized in the numbers.

Here’s what the numbers actually show.

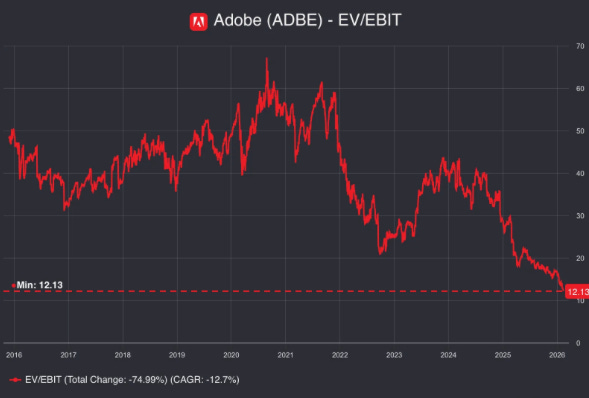

Adobe

The debate around Adobe is loud. Text-to-image, text-to-video, creative AI replacing Photoshop…you’ve heard it.

Here’s what’s harder to argue with. Since Adobe shifted to cloud in 2011, revenue went from $4.2B to $23.8B. Operating margins expanded from 26% to 37%. Average ROIC over the last decade: 31%. That’s more than triple the S&P 500.

The business got better every year while the debate raged. It’s now trading at its lowest earnings multiple in over a decade.

Constellation Software

Constellation acquires vertical market software companies. Over 1,000 of them. Software for cemetery mapping, chicken coop management, public transit scheduling. None of these are glamorous. That’s the point.

Small addressable markets mean limited competition for acquisitions. Constellation buys these businesses cheaply, runs them efficiently and compounds free cash flow at ROIC above 15% over ten years.

Shares have collapsed more than 50% in six months on fears that AI will “vibe-code” these businesses into obsolescence. For a serial acquirer with this track record, that’s a remarkable gift.

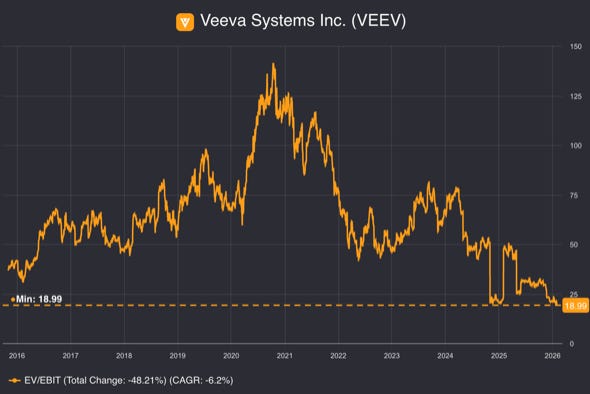

Veeva Systems

47 of the top 50 biopharma companies are Veeva customers. That number tells you almost everything.

Veeva builds cloud software for the life sciences sector. Purpose-built for stringent global regulations, clinical trial data management, drug commercialization. Switching to an unproven provider isn’t a risk biopharma companies take lightly. This isn’t a soft moat. It’s structural.

Revenue has grown from $61M to $3.1B. ROIC has averaged 37% since 2012. The stock has dropped 42% in four months. It’s now trading at its lowest multiple ever.

ServiceNow

Few companies describe their own market position as clearly as ServiceNow does: the central nervous system of the enterprise.

They’re not wrong. ServiceNow is the system of record across multiple departments in large organizations. Once embedded, it becomes foundational. That’s why renewal rates sit at 98%, among the highest of any global software company.

Since 2012, revenue grew from $244M to $13.4B. Free cash flow ROIC averaged 37% over the last decade. Free cash flow per share compounded at 31% annually.

The stock is down 57% from its peak. Largest drawdown in company history. $95B in market cap gone in four months.

The bear case is that AI enables in-house alternatives. Worth monitoring. But the renewal rate says customers aren’t leaving, and the financials say this business compounds exceptionally well.

The pattern here

Four category-dominant businesses. Decade-long ROIC above 30%. Now at multi-year or all-time low valuations.

The behavioral trap is availability bias, investors anchoring to AI disruption headlines instead of the underlying economics. When fear drives price, quality investors pay attention.

The question isn’t whether AI will change software. It will. The question is whether these specific businesses, with these specific moats, will still generate exceptional returns in ten years. The numbers suggest yes.

Seeing this pattern in your portfolio or deal flow? Reply and let’s work through the quality signals together.