Klarna: The $14 Stock That Can’t Decide If It’s a Bank

Klarna IPO’d in September 2025 at $40 per share. Six months later, on February 20, 2026, the stock closed at $13.09, down 25% in a single session. The company had just reported $1 billion in quarterly revenue for the first time in its history.

Think about that sentence for a moment. A company that grew Q4 revenue 38% year-over-year, to $1.08 billion, watched its stock hit an all-time low the same morning. The culprit was not fraud, not a product failure, not a competitive collapse. It was $250 million in provisions for credit losses. That number appeared in the income statement because Klarna is now, by any fair description, one of the largest consumer lenders in Europe with a fast-expanding US book.

That tension is the story. Not the headline numbers. The tension between what Klarna says it is and what its balance sheet says it is becoming.

Revenue per employee at Klarna reached $1.24 million in 2025, up from $344,000 in 2022. Headcount fell from 5,527 to 2,831 over the same period. These are among the most impressive productivity numbers of any financial services business anywhere. And yet the company posted a net loss of $273 million in the same year it achieved them. Because the other side of the ledger tells a different story: $794 million in provision for credit losses, $667 million in funding costs, $157 million in stock-based compensation. That cost structure belongs to a different kind of business entirely.

The market is not mispricing Klarna because it is dumb. It is mispricing Klarna because it is using the wrong mental model. The consensus frame is that Klarna is a capital-light fintech that briefly turned into a bank by mistake. My view is the reverse: Klarna is a bank wearing a fintech costume, and that is where the opportunity and the risk both sit.

The Behavioral Lens

The bias at work here is category anchoring, and it is operating on both sides of the trade.

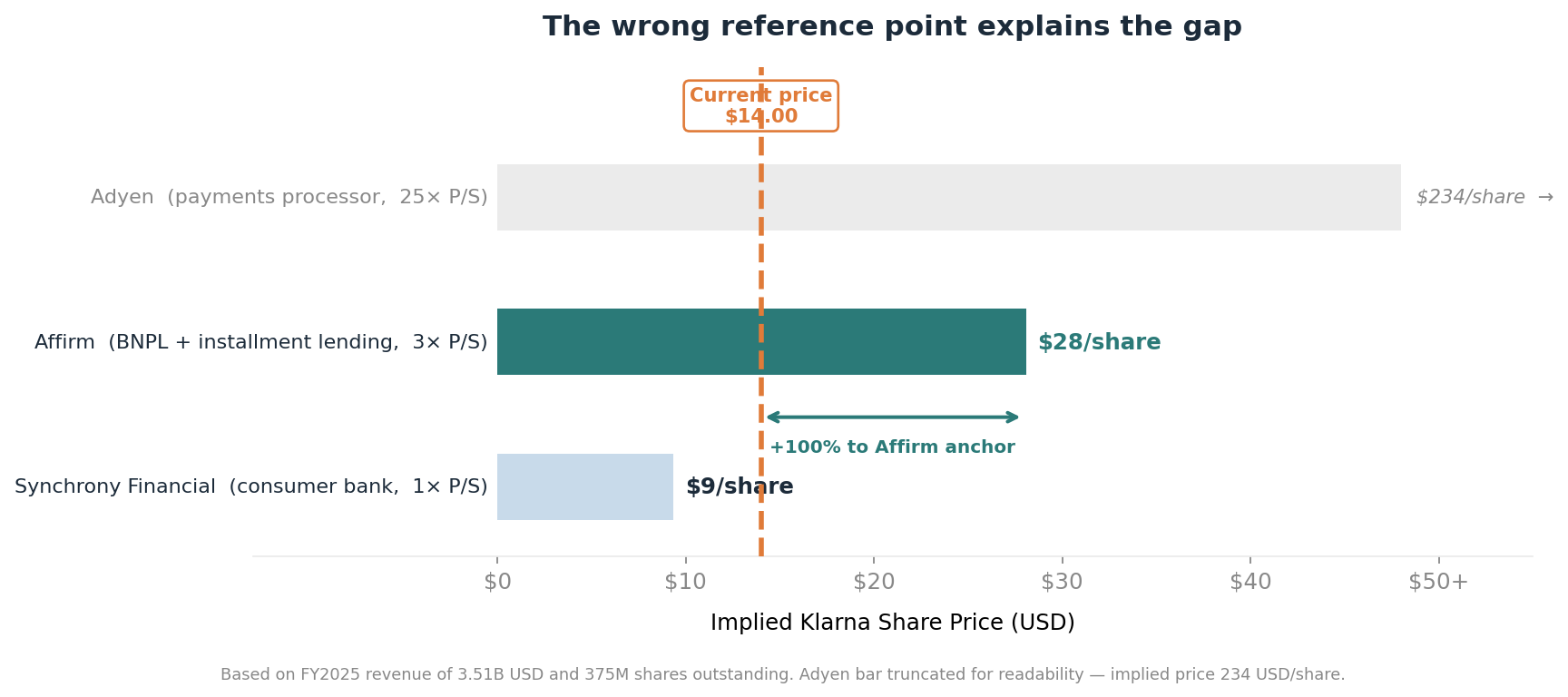

Kahneman documented the reference point problem decades ago: people reach for the nearest familiar category and price accordingly, even when the category is demonstrably wrong. Klarna is labeled a fintech. The fintech label triggers the Adyen comparison. Adyen trades at roughly 25 times revenue, generates zero credit losses, holds zero consumer deposits, and runs on interchange and gateway fees. Apply that multiple to Klarna’s $3.5 billion 2025 revenue and you get an $87 billion company. Nobody believes that. But the label keeps pulling in that direction.

The opposite anchoring is equally wrong. Call Klarna a bank and you trigger Synchrony Financial, which trades at roughly 1 times revenue and manages a $100 billion consumer credit book with 30 years of US underwriting experience. Apply that multiple to Klarna and you get a $3.5 billion company. Roughly where it traded on the morning of February 21, 2026.

Neither anchor is fully right. The least wrong comparison is Affirm: US-focused BNPL plus consumer installment lending, with a broadly similar revenue mix between merchant fees and interest income. Affirm trades at roughly 3 times forward revenue. At 3 times Klarna’s 2025 revenue, fair value sits around $10.5 billion, or roughly $28 per share.

That gap between $14 and $28 is not random. Category anchoring explains a meaningful part of it. Street bulls anchor on Adyen because it keeps the fintech dream alive. Bears anchor on Synchrony because it lets them call Klarna just another subprime lender. Both are emotionally convenient and analytically wrong. In behavioral terms, the contrarian stance here is not about buying what is down. It is about refusing the wrong reference point altogether. The rest of the gap is genuine uncertainty about whether Fair Financing credit quality holds.

Klarna is a bank with a fintech multiple, fighting to become a fintech with a bank balance sheet. That tension is what the stock price reflects.

In the deals I have analyzed where businesses simultaneously occupy two value frameworks, part capital-light platform and part balance sheet lender, the market consistently misprices the compound entity until one cycle forces a reclassification. You saw the same dynamic play out with PayPal in the years after its spin from eBay, and with Square as it built Cash App on top of its payment rails. The reclassification is almost always painful for whoever was using the higher-multiple anchor. Klarna’s Q4 results were that reclassification moment. The question now is whether the market overshoots to the low-multiple anchor, which at $12.50 intraday on February 21 it may have done.

The Team

Sebastian Siemiatkowski co-founded Klarna in 2005, at 25 years old, with Viktor Jacobsson and Niklas Adalberth. Jacobsson and Adalberth have long since stepped back from operations. Siemiatkowski has been running the company for twenty years, through the 2008 crisis, through the 2022 $45 billion valuation that collapsed to $6.7 billion within twelve months, and through the 2025 IPO that reversed much of the same ground.

He is not a defensive CEO. The decision to cut 700 employees in 2022, and then another 10% in 2023, while simultaneously betting the company on AI-driven productivity, was not a committee consensus. It was a unilateral call that looked reckless at the time and looks prescient now. Revenue per employee nearly quadrupling in three years is the outcome.

CFO Niclas Neglén joined in 2024. One full year of profitability followed. Then an IPO roadshow that presented Klarna as a business that had turned the corner. Then a $273 million net loss in the first year as a public company.

The timing of the CFO appointment and the IPO narrative creates an uncomfortable question. One plausible reading is that the 2024 profitability ($21 million net income) partially reflected a deliberate pacing of Fair Financing growth to present a cleaner P&L before listing. The $250 million Q4 provision spike, triggered by accelerating Fair Financing adoption at a near 200% exit rate, suggests the underlying lending demand was always there. It was a timing choice, not a structural breakthrough.

This is the question at the center of three class action lawsuits filed against Klarna post-IPO, alleging misrepresentation of loss reserves. Klarna denies the allegations. The lawsuits are worth watching not because they will prevail (they usually do not), but because the discovery process occasionally surfaces documents management would rather not discuss publicly.

The Glassdoor signal deserves a line. At the time of writing, Klarna’s employee rating sits at 3.0 out of 5.0, against a financial services industry average of 3.7. Only 37% of employees would recommend the company. The most consistent recent theme in reviews: anxiety about constant layoffs. A company driving productivity by sustained headcount reduction creates a specific cultural dynamic. The people who remain are working harder. The people being displaced are angry. The numbers look good until morale becomes the bottleneck.

The Business Model and Go-to-Market

There are two businesses inside Klarna. They share a brand, a balance sheet, and 100 million customers. Their economics have almost nothing in common.

Business one: BNPL and payments. Zero-interest installment products (Pay in 4, Pay in 30) where Klarna charges the merchant a discount rate of roughly 2 to 3 percent of transaction value. The merchant pays because Klarna reduces cart abandonment and increases average order value. Klarna absorbs limited credit risk on these products: the loans are 6 to 8 weeks in duration, and the charge-off rate sits at approximately 0.6 percent of receivables. This business generated $2.5 billion in transaction and service revenue in 2025. It is capital-light, operationally scalable, and structurally high quality. It is why the fintech label stuck.

Business two: Banking and Fair Financing. Interest-bearing installment loans with 12 to 24 month terms. Consumer deposit accounts. The Klarna card. Revenue from interest income ($937 million in 2025), deposit spread, and loan sales (a new line item as of Q4 2025). This business is growing fast: Fair Financing receivables grew 165% year-over-year in Q4. Banking customers reached 15.8 million, up 101%. The average revenue per banking customer is $107, versus $30 for the overall base. This is the high-value segment.

It is also where every provision dollar sits.

The go-to-market for business two is business one. Klarna acquired 100 million consumers through the frictionless BNPL checkout experience, which was essentially a customer acquisition loss leader, and is now monetizing those relationships with longer-duration financial products. The unit economics on the second sale are exceptional: zero marginal acquisition cost on an existing user who already trusts the brand. This is the strategic logic. It is sound.

The execution question is whether Klarna can underwrite 12-month US consumer loans better than Capital One, which has been doing it since 1994.

Competition and Positioning

Klarna’s original BNPL market is contested from three directions that will only intensify.

Affirm is the direct US analog and the benchmark that matters most. Affirm has deeper partnerships (Amazon, Shopify) and a longer track record of US consumer credit underwriting. The recent addition of Walmart to Klarna’s US network is the most meaningful competitive move Klarna has made: Walmart’s consumer base is lower-income, higher-credit-stress, and enormous. That combination will tell you more about Klarna’s US Fair Financing credit quality in the next four quarters than any model can.

Klarna’s 850,000-strong merchant network is roughly twice Affirm’s 478,000 and took fifteen years to build. Sezzle discovered this the hard way: it attempted to construct a competing network, stalled at around 50,000 merchants, and eventually pivoted to monetizing consumers directly through subscriptions rather than continue trying to sign merchants who already had Klarna and Affirm available. The economics of double-sided payment networks tend toward oligopoly for the same reason card networks do: fragmentation creates friction that neither side will tolerate. That structural reality is what makes Klarna’s merchant base more durable than it looks on a spreadsheet.

The competitor Klarna is underestimating is not Affirm. It is Capital One, assuming its announced Discover acquisition clears final regulatory review. Capital One has 100 million existing US credit card customers, would own the second-largest credit card network in the US, and is already building its own installment product inside a credit card wrapper. They do not need Klarna’s merchant relationships. They already have the customers. They have 30 years of subprime underwriting data that Klarna is currently building from scratch. And their installment product sits inside a credit card statement the consumer is already opening every month.

On the banking side, the relevant threat is Revolut, which has a much stronger brand proposition in Europe and is targeting the same banking-as-an-engagement-tool strategy. Revolut had 50 million users as of mid-2025. Klarna has 100 million. The gap is closing. And Revolut does not carry the credit risk of a lending book on its balance sheet.

None of this makes Klarna’s competitive position hopeless. Merchants choose Klarna at checkout because it demonstrably lifts conversion and average order value in ways a bank-issued card product does not. That demand generation argument survives Capital One. It does not survive Capital One plus the full Discover merchant network at lower MDR. Klarna’s current positioning is a real asset: the most recognized BNPL brand globally with a genuine AI productivity advantage. The moat is real for the payments side. For the banking side, the moat is unproven.

The Financials

Revenue grew from $2.81 billion in 2024 to $3.51 billion in 2025, a 24.8% increase. Q4 revenue hit $1.08 billion, up 38.5% year-over-year. These are strong numbers.

Everything below revenue is more complicated.

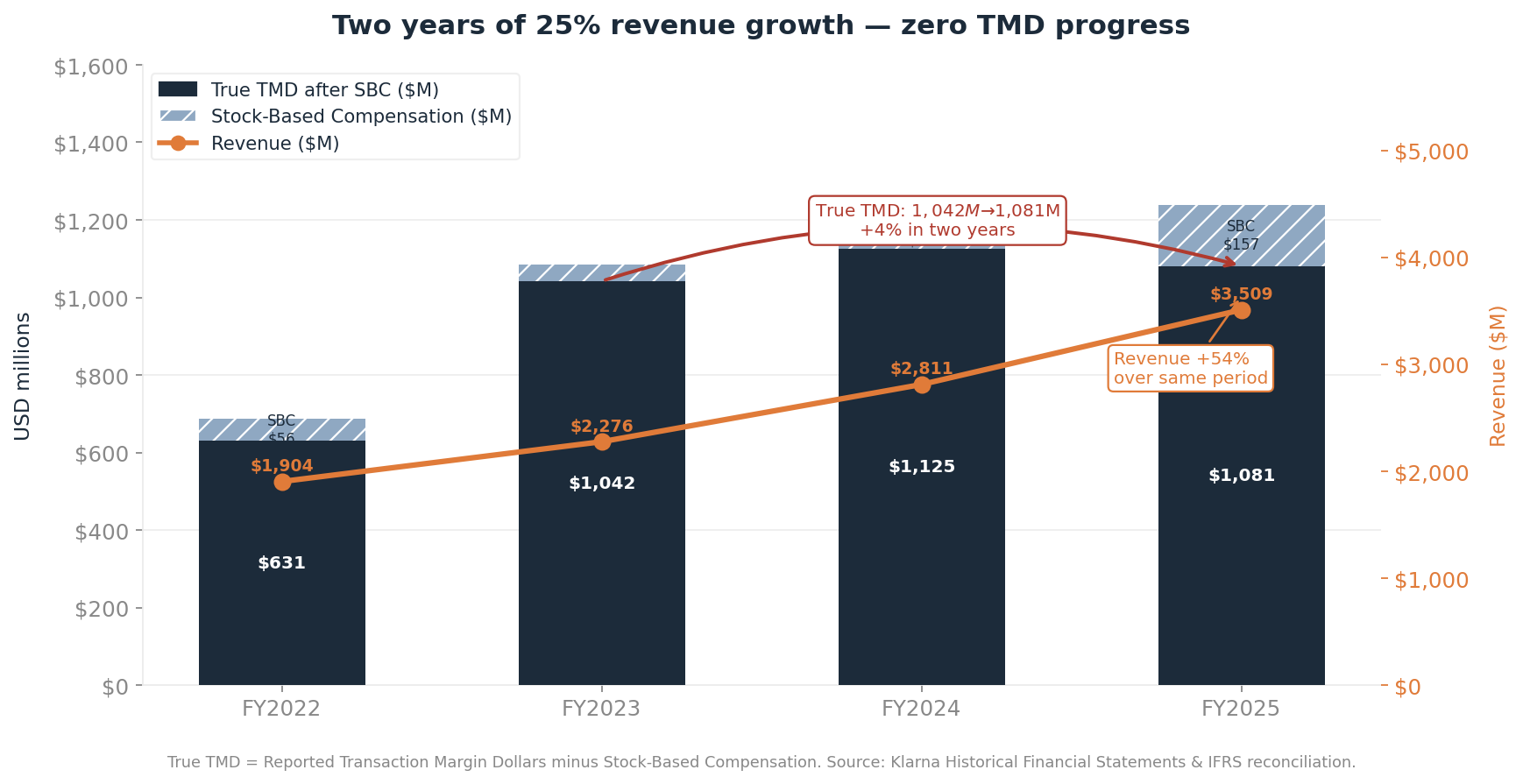

Transaction Margin Dollars (Klarna’s preferred operational metric, defined as revenue minus processing costs, credit loss provisions, and funding costs) grew from $1.217 billion in 2024 to $1.238 billion in 2025. That is 1.7% growth in the metric that should be compounding fastest. Management guided Q4 TMD at $390 to $400 million. Actual Q4 TMD came in at $372 million. This was Klarna’s first quarter as a public company in which it had provided formal guidance. It missed.

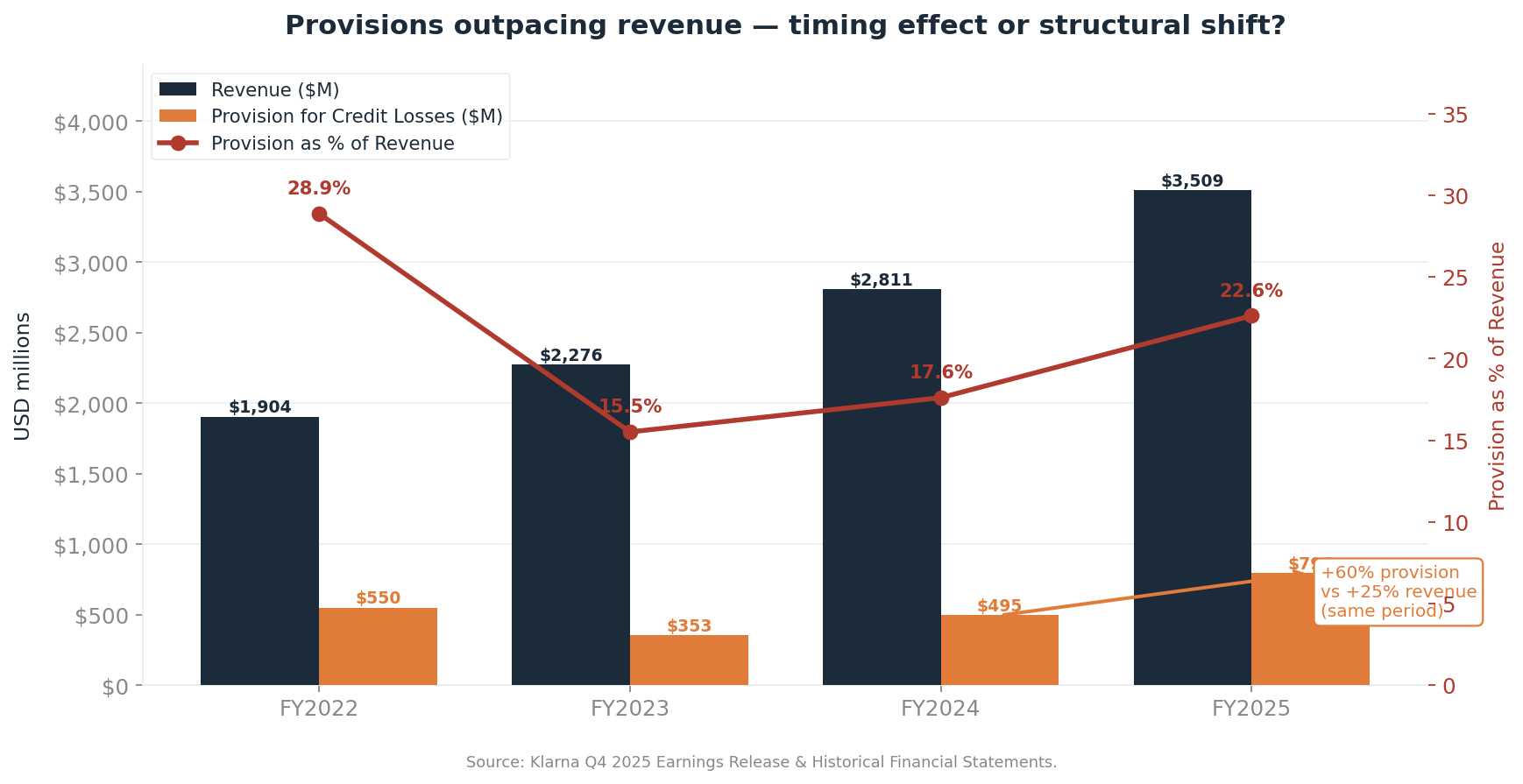

Provision for credit losses: $353 million in 2023, $495 million in 2024, $794 million in 2025. The increase from 2024 to 2025 is 60.4%. Revenue grew 24.8% over the same period. This divergence is the single most important number in the whole filing and it receives less than a page of disclosure.

Management’s explanation is mechanically correct. Under CECL accounting rules, US companies must provision for the lifetime expected credit losses of a loan at origination, not as losses actually materialise. Klarna originated a $2.5 billion US Fair Financing portfolio in Q4 2025, per management commentary, growing at a near 200% annualized exit rate. On that portfolio, Klarna booked most of the lifetime expected credit loss provision in the current quarter while recognizing only a fraction of the lifetime interest income today. The bulk of the spread accrues over the following 12 to 24 months. The provision was front-loaded; the revenue was not.

This is the legitimate bull case. If the CECL provisioning assumptions are correct, meaning actual charge-off rates stay below 2.5%, then the front-loaded provisions become future profit as the portfolio seasons. The mechanical drag on TMD in H2 2025 reverses into a tailwind in H1 2026, TMD recovers to $1.4 to 1.5 billion, and the company looks profitable again. The bear case is simpler: the CECL assumptions were too optimistic, actual losses run above them, and the provisioning drag does not reverse. It compounds.

The number management is not foregrounding: true TMD after stock-based compensation. Reported TMD in 2025: $1.238 billion. SBC in 2025: $157 million, up from $92 million the prior year, a 70.7% increase. True TMD after SBC: $1.081 billion. That number has been essentially flat since 2023, when actual TMD was $1.085 billion. Two years of revenue growth at 25% per year, and the core operational metric, once you include the real cost of retaining talent through equity, has not moved.

Available vintage data on US Fair Financing shows cumulative charge-off rates ranging from 2% to 4.5% across post-2022 cohorts. The CECL reversal thesis works at the lower end of that range. At the upper end, provisions were optimistic rather than conservative, and the math reverses. That range is the honest bandwidth of uncertainty — not a range where all outcomes are equivalent.

One data point that works in the bull case’s favour: when Klarna sold $1.6 billion of Fair Financing receivables in Q4, it recorded a $73 million gain above book value. An arm’s-length secondary buyer paid a premium for the paper. That is an independent credit quality signal that no internal disclosure can replicate, and the market has largely ignored it. The same analysis applies to the underlying funding economics: against the provision drag, the lending engine itself generates a positive $512 million net interest spread, with $937 million of interest income against $425 million of funding costs. The engine works. The drag is accounting mechanics, not a broken spread.

The metric to watch over the next two quarters is the Fair Financing net charge-off rate. It is not yet separately disclosed. When it is, and if it comes in below 2.5%, the CECL thesis holds and the path to profitability is real. If it exceeds 3.5%, the provisions were optimistic, not conservative, and the loss trajectory worsens.

Where the Quality Is (and Where It Is Not)

The quality is genuine on the operating side.

Revenue per employee of $1.24 million in 2025 is not a one-year artifact. It is the result of a three-year commitment to AI-driven automation that started before the AI wave was fashionable. Klarna reduced its customer service headcount from thousands to hundreds using AI agents, with equivalent or better resolution rates. Stripe’s revenue per employee, by comparison, is approximately $800,000. Klarna is running ahead of one of the best-operated businesses in fintech on this metric.

The 100 million active consumer relationships are a real asset. The brand in Europe, particularly in the Nordic markets and Germany, is a genuine moat, the kind of top-of-mind payment method that requires a decade of habit formation to build and is extremely sticky once established. Net Promoter Score data is not publicly available, but the Trustpilot volume (over 400,000 reviews, predominantly positive) at least suggests no broad consumer exodus.

Banking customer ARPU at $107 versus $30 for the overall base shows the monetization potential of the banking pivot is real, not theoretical.

The quality is not present in three places.

Guidance credibility: missing TMD guidance by 4.5% to 7% in the first quarter as a public company is not a catastrophe. It is a yellow flag that becomes red if it repeats. Compass Point called the high end of 2026 TMD guidance “unbelievable.” That word, from a sell-side analyst who maintains a Buy rating, is notable.

Earnings quality: operating cash flow in 2025 was negative $1.032 billion, driven by $2.787 billion in consumer receivables growth and $852 million of debt securities investment. The business is consuming cash at scale to fund its lending book. That is expected for a growing lender. It is not the cash profile of a capital-light platform, which is what the IPO roadshow implied.

Capital allocation discipline: stock-based compensation tripled between 2023 and 2025 (from $43 million to $157 million). Against reported TMD of $1.238 billion, that is a 12.7% dilution of the primary operational metric. Against the Adjusted Operating Profit of $65 million (2025), SBC exceeds operating profit by 2.4 times. The reported profitability is an accounting construction; the cash cost of running this business, including its people, remains negative.

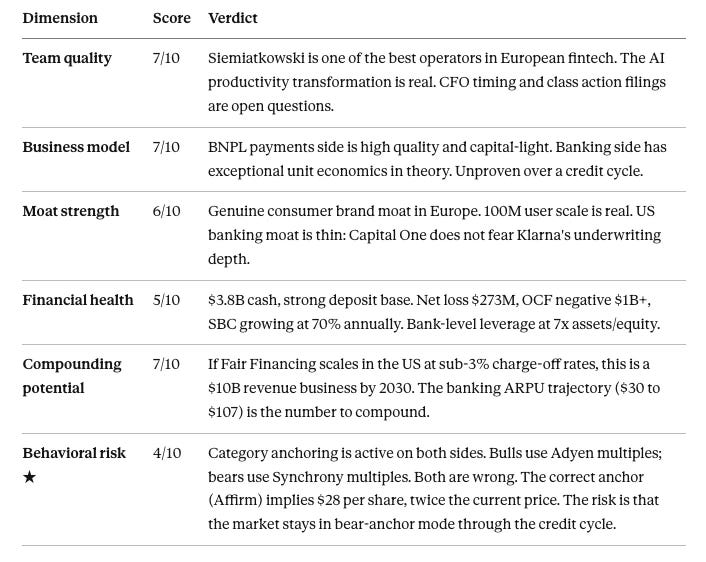

The Quality Scorecard

Total: 36/60. Conditional quality. The core business is real. The path to profitable scale exists. Two critical uncertainties must resolve: US Fair Financing credit quality and guidance credibility. Until both improve, the scorecard stays here.

The Bold Call

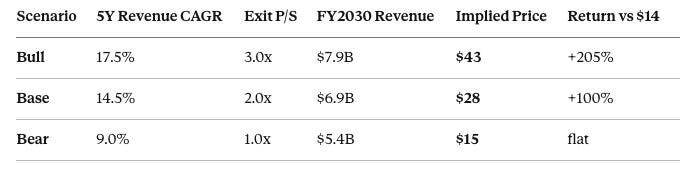

A reverse DCF from current price is instructive. At $14/share and 375 million shares outstanding, the market is effectively pricing in roughly 11.5% revenue CAGR over five years at a 1.5x exit P/S multiple — a scenario that already implies a share price of approximately $21. The market is pricing Klarna as if revenue growth stalls to near-bank levels while simultaneously applying a near-bank valuation. That combination requires both the bear anchor and the growth pessimism to be right at the same time.

The three-scenario model below runs five years to FY2030 using a WACC of 11.75%:

The bear case showing flat rather than deeply negative is itself a finding. Klarna holds $3.8B in corporate cash against $1.4B in notes payable, a $2.4B net cash position worth roughly $6.50 per share. Even at a 1.0x revenue exit multiple, near bank-level distressed pricing, the cash buffer prevents outright capital destruction. The bear case risk is not losing 40% of your money. It is holding a stock that goes nowhere for five years while opportunity cost accumulates. That is a meaningful distinction for how you size the position.

The asymmetry is real: the bull case more than triples your money; the bear case roughly preserves it; the base case doubles it.

Scenario A (Bull): Fair Financing net charge-off rates stay below 2.5% through 2026. CECL front-loading from Q3/Q4 2025 reverses into a $200 million tailwind on TMD in H1 2026. TMD reaches $1.55 billion for the year. Banking customers reach 25 million, ARPU expands further. Elliott’s $6.5 billion forward flow agreement scales smoothly. Revenue compounds at roughly 17-18% annually to $7.9B by FY2030. At a 3.0x P/S exit, the Affirm-parity case, implied price is $43 per share (+205%).

Scenario B (Base): Charge-off rates settle at 2.5 to 3%. CECL front-loading normalizes but does not fully reverse. TMD reaches $1.4 billion, roughly in line with 2026 guidance midpoint. Revenue compounds at roughly 14-15% annually to $6.9B by FY2030. Company reaches break-even profitability by end of 2026. At a 2.0x P/S exit, implied price is $28 per share (+100%).

Scenario C (Bear): US consumer stress accelerates in 2026, driven by tariff-related inflation and resumed student loan payment pressure. Fair Financing charge-off rates reach 4 to 5%, a genuine stress scenario that exceeds CECL assumptions materially, not marginally. Klarna pulls back lending, revenue growth slows to roughly 9% annually to $5.4B by FY2030. At a 1.0x P/S exit, the cash-adjusted floor produces an implied price of $15 per share (flat).

My call is Scenario B, with a near-term caveat that overrides all of the above.

March 9, 2026, eleven days from today, is the lock-up expiration date. 335.5 million shares become freely tradeable. At $14 per share, that is $4.7 billion of potential selling into a market cap of $5.3 billion. This is not a normal lock-up event. This is a near-total float refresh. The stock is likely to be under pressure, whatever the fundamentals say, until this overhang clears. The academic literature on lock-up expirations is consistent on this: abnormal negative returns cluster around expiry dates even when the expiry is fully anticipated and priced, because supply effects and signalling effects compound. The street knows March 9 is coming. That does not mean the selling will be orderly.

The one metric I will watch to know if I am wrong: Q1 2026 Fair Financing net charge-off rate, reported in May 2026. Below 2.5%: base case holds, the CECL argument is real, and I would be inclined to accumulate after the lock-up clears. Above 3.5%: bear case escalates, the provisioning was optimistic, and the entire lending expansion thesis must be revised.

If I’m wrong, it’s because of one of two things.

First: Fair Financing charge-off rates come in above 3.5% in Q1 2026. That invalidates the CECL-mechanics bull case entirely and turns the provision trajectory from a timing issue into a structural one. I will update this view in writing the moment that data is public.

Second: the Affirm anchor is itself wrong. If Affirm’s multiple compresses from 3x to 1.5x as markets re-price installment lending credit risk broadly, the fair value calculation for Klarna compresses with it and the $28 target disappears. Watch Affirm’s Q3 2026 credit results as a leading indicator for Klarna’s.

If you are underwriting US consumer credit or running a BNPL or installment book, I especially want to hear from you. The central question is whether the 2025 provision spike is CECL mechanics or genuine credit deterioration. Those two explanations produce completely different conclusions about fair value.

And if you think Klarna deserves an Adyen-style multiple, tell me why the balance sheet should trade at a payment-processor risk premium. I have not found a satisfying answer. Maybe you have.

Sources: Klarna Group plc Q4 2025 Earnings Release; Klarna Historical Financial Statements Q4 2025; Klarna Q4 2025 Investor Presentation; Klarna Holding AB H1 2025 Financial Statements; Morgan Stanley analyst note (February 2026); Compass Point Research; Bernstein Research; Seeking Alpha; NBC News; Fortune; Consumer Financial Protection Bureau.

Disclosure: No current position in Klarna Group plc at time of publication.