Kelly Partners Group: Good Business, Dangerous Narrative

Ticker: ASX: KPG Current Price: Around AUD $6.00 (as at March 2026) All-Time High: AUD $13.60 (February 2025) Analyst Consensus Target: AUD $4.70-4.90 Qapital Rating: CAUTIOUS

The Pitch Everyone Heard

If you subscribe to micro-cap research newsletters, you have almost certainly encountered Kelly Partners Group. The story is compelling and it is told well. Brett Kelly, founder, CEO, and 47% owner, built an accounting firm aggregator from scratch in 2006, identified a structural gap before anyone was talking about it, and has since grown revenue dramatically. He references Berkshire Hathaway. He references Constellation Software. He publishes an Owners’ Manual, now in version 4.0. He talks about permanent capital, long-term thinking, and alignment. The share count is actually lower than at IPO. The business has been compounding for two decades. William Thorndike, the author of The Outsiders, is a shareholder. Lawrence Cunningham sits on the board.

Micro-cap analysts, especially those charging a hefty subscription fee to deliver conviction ideas, love all of this. The narrative is tight, the founder is credible, and the concept is differentiated. Kelly Partners has been featured on paid platforms, Substack newsletters, and investor conferences as the kind of quietly exceptional business that institutional investors overlook. The community around the stock has been vocal and enthusiastic.

The community is not wrong about everything. Brett Kelly has built something real. The model is genuinely unusual. The business does generate cash. The client satisfaction numbers are remarkable: KPG reports a Net Promoter Score of 72, against an industry average of negative 18. That is not a marketing number. That reflects something genuinely working at the practice level.

But between a good business and a good investment sits a dangerous gap. That gap is where we want to spend our time today.

The Machine Itself

Understanding Kelly Partners requires understanding how it actually makes money, because the structure is more complex than it appears.

Kelly Partners does not simply buy accounting firms. It acquires a 51% controlling stake in owner-operated practices (typically paying around six times post-implementation cash flow) while the existing partners retain the remaining 49%. The seller becomes a minority partner. They keep their name on the door, continue running client relationships, and retain meaningful financial upside through their equity stake. In return, they gain access to Kelly’s centralised back-office, technology infrastructure, HR, and brand.

Each operating company (opco) pays a management fee of 9% of its revenue to the parent entity (6.5% for central services, 2.5% for intellectual property). This fee funds KPG’s corporate centre and generates the return that flows to public shareholders. The operating partners service their local acquisition debt (typically two-thirds funded by banks, one-third by vendor loans) while the parent consolidates all subsidiary revenue into its reported group figures.

One genuine discipline worth acknowledging: KPG operates with no formal revenue targets, no profit targets, and no acquisition deadlines. Brett Kelly has been explicit that this is intentional. Deals are done when they are right, not because a quarter needs filling. This reduces the pressure to do bad acquisitions that has destroyed many rollups.

The pitch is that this structure solves the fundamental problem of professional services rollups: culture destruction. When a large firm acquires a small practice outright, the founding partners cash out, lose motivation, and client relationships gradually erode. Kelly’s 49% retention keeps founders invested. The 10-year partnership agreements create horizon-matching. On paper, it is elegant.

In practice, it is more complicated. KPG consolidates 100% of subsidiary revenue (despite owning only 51%) and then strips out minority interests below the EBITDA line. This creates a revenue figure that flatters the parent’s scale, while the earnings attributable to KPG shareholders are materially smaller than the consolidated top line implies. The opco pays 9% to KPG regardless of whether it is growing or shrinking. That royalty structure is fine when times are good. When organic growth stalls, that 9% drag creates tension between the parent extracting its fee and partners whose distributable cash is declining.

What the Revenue Chart Doesn’t Tell You

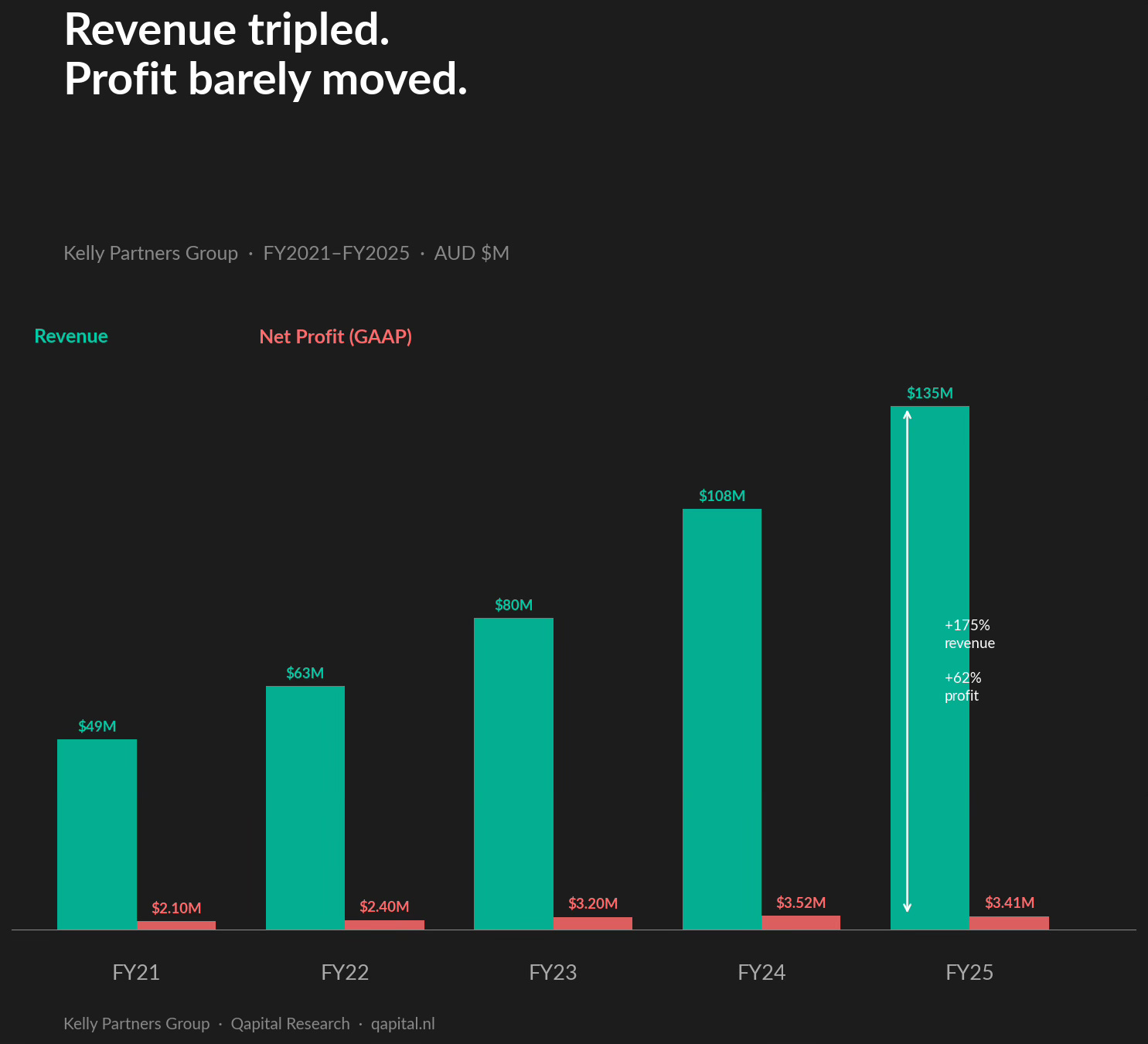

The headline number for Kelly Partners is impressive. Revenue reached AUD $134.6 million in FY2025, up 24.5% on the prior year and roughly triple where the business stood in the early 2020s. The H1 FY2026 result extended the run with another 17% growth to AUD $76 million, pushing the annualised revenue run rate to AUD $164 million. On a chart, this looks like a compounder.

But revenue is not earnings. And the earnings chart looks very different.

In FY2025, Kelly Partners reported statutory net profit attributable to shareholders of AUD $3.41 million. Revenue had grown 24.5%. Earnings declined approximately 3%.

In H1 FY2026, statutory net profit attributable to shareholders fell a further 4-5% year-on-year. Revenue was up 17%.

To restate: revenue tripled, profit shrank. Looking further back, EPS has declined on a five-year view. The company that newsletters describe as a compounder has, by the most honest measure available, compounded its revenue and eroded its earnings per share.

The net profit margin in FY2025 was 2.5%, down from 3.1% the year prior. For context, a well-run single-site accounting firm typically earns 20-30% EBITDA margins and converts much of that into profit. Kelly Partners earns 28% EBITDA margins at the underlying level but delivers 2.5% statutory net margins to parent shareholders. The gap between those two numbers is where the rollup cost hides.

Bulls will point to group-level free cash flow, which looks considerably better when you include the 49% owned by operating partners. That is a legitimate number, but it is not the return flowing to ASX shareholders. The distinction matters.

The NPATA Question

Kelly Partners does not lead with GAAP earnings. Its preferred performance metric is NPATA: Net Profit After Tax and Amortisation. In H1 FY2026, NPATA attributable to parent shareholders grew 12.8% to AUD $5.6 million. The company calls this its “true” earnings measure and builds most of its investor communication around it.

The logic behind NPATA is standard rollup thinking: when you acquire a business, you are required under accounting rules to recognise the value of customer relationships, brand, and other intangibles on the balance sheet, then amortise them over time. This amortisation charge is non-cash and does not represent a real ongoing cost, the argument goes. Strip it out and you get a cleaner picture of underlying earnings power. KPG discloses the full reconciliation transparently, so there is no question of concealment.

There is a version of this argument that is defensible. Depreciation of physical assets does involve real capital replacement costs that amortisation does not. In software businesses, similar arguments about capitalised development costs are well established. The Constellation Software analogy the bulls reach for is genuinely apt in some respects.

But in an accounting firm rollup, the argument is much weaker. When Kelly Partners buys an accounting practice for six times cash flow, it is paying for the client relationships of that firm. Those clients are human beings with accountants they trust. They are not locked in by software contracts or network effects. They churn. They retire. They get poached. The amortisation of those customer relationship intangibles is not an accounting fiction. It is a reasonable attempt to reflect the genuine economic decay of what was purchased.

More importantly: in a rollup that must continuously acquire to sustain its growth, the amortisation expense of past acquisitions is being replaced by the acquisition cost of new ones. Stripping out amortisation while simultaneously funding replacement acquisitions with debt presents a flattering, rather than complete, picture of earnings.

To illustrate the gap: FY2025 underlying NPATA attributable to shareholders was AUD $9.1 million, giving a P/NPATA multiple of around 30 times at current prices. Using the higher H1 FY2026 annualised NPATA of approximately AUD $11.2 million brings that to around 25 times. Both are materially different from the GAAP P/E of around 80 times. The gap between those figures is almost entirely acquisition amortisation. That is not a mirage. It is the real cost of the strategy.

Management has set an internal target of reaching AUD $40 million in NPATA by 2031. We will return to what that implies in the valuation section.

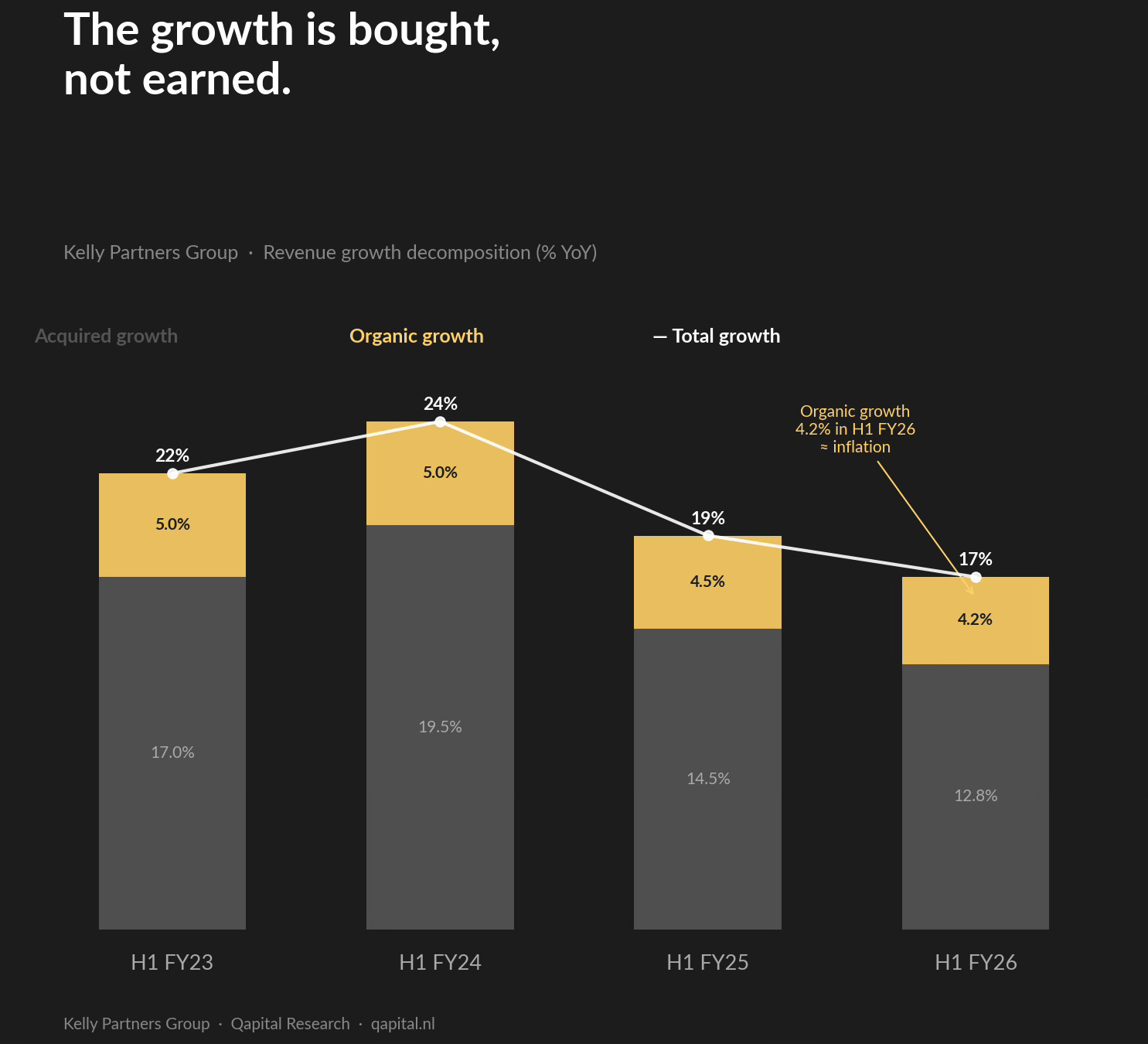

Organic Growth: Four Percent

Remove the acquisitions and ask a simple question: how fast is Kelly Partners growing?

The answer, from the company’s own reporting, is 4.2% in H1 FY2026 and 4.5% for FY2025. Organic revenue growth in the low single digits.

Australian CPI inflation for the same period ran at approximately 3-5%. On a real (inflation-adjusted) basis, the organic business of Kelly Partners is only slightly positive after inflation, and in some periods effectively flat.

Bulls counter this with a compelling argument: KPG’s clients currently access only around 10% of the services they could potentially use. The upsell runway within the existing client base is enormous, covering international tax, advanced structuring, wealth management, and risk management. If KPG can shift clients from compliance-only to advisory relationships, organic growth could accelerate materially without a single new acquisition.

This is a legitimate bull case. But it is also a promise, not a fact. Five years of reported organic growth in the 4-5% range suggests the upsell opportunity has not yet translated into numbers. Until it does, four percent is the baseline.

This matters enormously for how you should think about the equity value. A 4% nominal organic grower in a professional services business trades at a modest multiple: typically 8-12 times EBITDA for private transactions, perhaps 12-15 times for a listed entity with good management. The revenue growth is real but it is bought, not earned. Every percentage point above 4% is leverage and acquisition cost, not operating leverage.

The Acquisition Treadmill

Here is the mathematical problem with rollup models that compound investors sometimes gloss over: as you get bigger, you need more deals.

In H1 FY2026, Kelly Partners completed six acquisitions contributing approximately 12.8% to revenue growth, or roughly AUD $9.8 million of incremental acquired revenue on a base of AUD $76 million.

As the company’s revenue base grows, it needs progressively more acquired revenue to maintain the same percentage contribution from M&A. As an illustrative scenario: by FY2028, with a revenue base approaching AUD $200 million, maintaining 12-13% acquisition contribution would require finding and integrating meaningfully more acquired revenue than today, at a higher deal cadence.

The management NPATA target of AUD $40 million by 2031 makes this dynamic explicit. FY2025 underlying NPATA to the parent was AUD $9.1 million. Reaching $40 million in six years requires approximately 28% annual NPATA growth. Given that organic revenue growth is running at 4%, almost the entire NPATA uplift must come from a dramatically accelerating acquisition machine combined with significant margin expansion. Management says margins can move from around 15.5% toward 32.5%, but no timeline or mechanism for that improvement is publicly detailed.

This is not impossible. Brett Kelly claims demand from firms wishing to join “has never been stronger.” The baby boomer retirement wave is real. The succession crisis across the 87,000 firms facing ownership transitions in Australia, the US, and the UK is genuine. But the market is not infinite. The better firms will be acquired first, leaving lower-quality or higher-priced targets in subsequent years. Competition from other aggregators, including private equity, which has noticed the same opportunity, pushes acquisition prices up over time. Net debt has already risen 32% in a single half-year to AUD $77.1 million at 1.79 times EBITDA, with the DayPriest Investor research flagging balance-sheet creep as the key risk to watch.

The treadmill does not stop. It only speeds up. The $40 million NPATA target is an ambitious plan. The question is whether it is a realistic one given the current organic growth rate.

The AI Question

There is a structural risk in the Kelly Partners thesis that the bull community has begun to grapple with, and its conclusions are more nuanced than either the bears or the bulls fully acknowledge.

The practices Kelly Partners buys derive a significant portion of their revenue from tax compliance, bookkeeping, payroll processing, and similar recurring services to small and medium-sized private businesses. These are precisely the service categories that AI agents are targeting. Xero and MYOB have already automated large parts of bookkeeping. AI-driven tax preparation tools are emerging across every major market. Research cited by a bullish KPG analyst suggests AI could handle 20-50% of such routine tasks by 2030. Even in a bullish framing of AI, that is a significant compression of the billable hour at the low end.

The genuine counterargument, which deserves serious weight, is regulatory complexity. The Australian tax environment is becoming measurably more complex: superannuation tax changes, personal services income provisions, trust distributions, fringe benefits, payday super, and AML extensions to accountants are all adding to the compliance burden rather than reducing it. The ATO is also intensifying enforcement, which drives more businesses toward professional advice. Complexity and compliance create demand, and that demand is not obviously reducible to software.

The honest assessment is that AI represents a headwind to low-value compliance volume and a potential tailwind to high-value advisory. The question for KPG is whether its practices are positioned to capture the advisory upside. The 4% organic growth figure does not yet suggest they are. If firms can make the transition, the AI impact may be net neutral or even positive. If they cannot, the recurring revenue value of the practices being acquired today is lower than the acquisition price implies.

KPG’s recent acquisition of WrkPod, an outsourcing business, introduces additional uncertainty about whether all parts of the portfolio are equally defensible.

The US Gamble

Kelly Partners entered the United States in 2023, with Brett Kelly personally relocating to Los Angeles to lead the expansion. Offices have been established in California and Florida, with further presence in Texas and North Carolina. US operations now represent approximately 12-15% of group revenue. The company has positioned the US expansion as a multi-decade growth opportunity: a second, much larger version of the Australian playbook.

The most prominent US client relationship disclosed is the provision of accounting services to a Florida-based firm serving approximately 700 McDonald’s franchisees, representing roughly 5% of the entire US McDonald’s franchise network. This is real and recurring work, and it demonstrates genuine sector specialisation in a client pool with predictable, complex financial needs. It is a stronger proof of concept than it might initially appear.

The broader question remains: demonstrating that you can serve McDonald’s franchisees in Florida well does not demonstrate that you can replicate the Australian partner-owner model across fifty state jurisdictions with different regulatory, tax, and cultural environments. The Australian model took nearly two decades to build to over 100 operating partners. The US market is vastly larger, more fragmented, and more competitive. Building a similar network there, while simultaneously servicing Australian growth and incurring the debt to fund both, is a meaningful execution risk.

US margins are not disclosed separately from the Australian results. We do not know whether the US operations are currently profitable on a standalone basis. For a company deploying debt to fund both geographies, this is an important information gap.

Governance Note

In early 2026, a former executive of Kelly Partners filed a civil lawsuit against the company. The claim alleges a bonus dispute, and the executive reportedly stated they resigned due to “fear for their safety.” These are allegations only, have not been tested in court, and the company has not made detailed public comment.

We include this not to sensationalise it, but because investors in a founder-led business with significant key-person concentration should be aware of legal proceedings that may reveal something about internal culture, even if the ultimate outcome is routine. The lawsuit does not change our fundamental thesis, but it is material to the full picture.

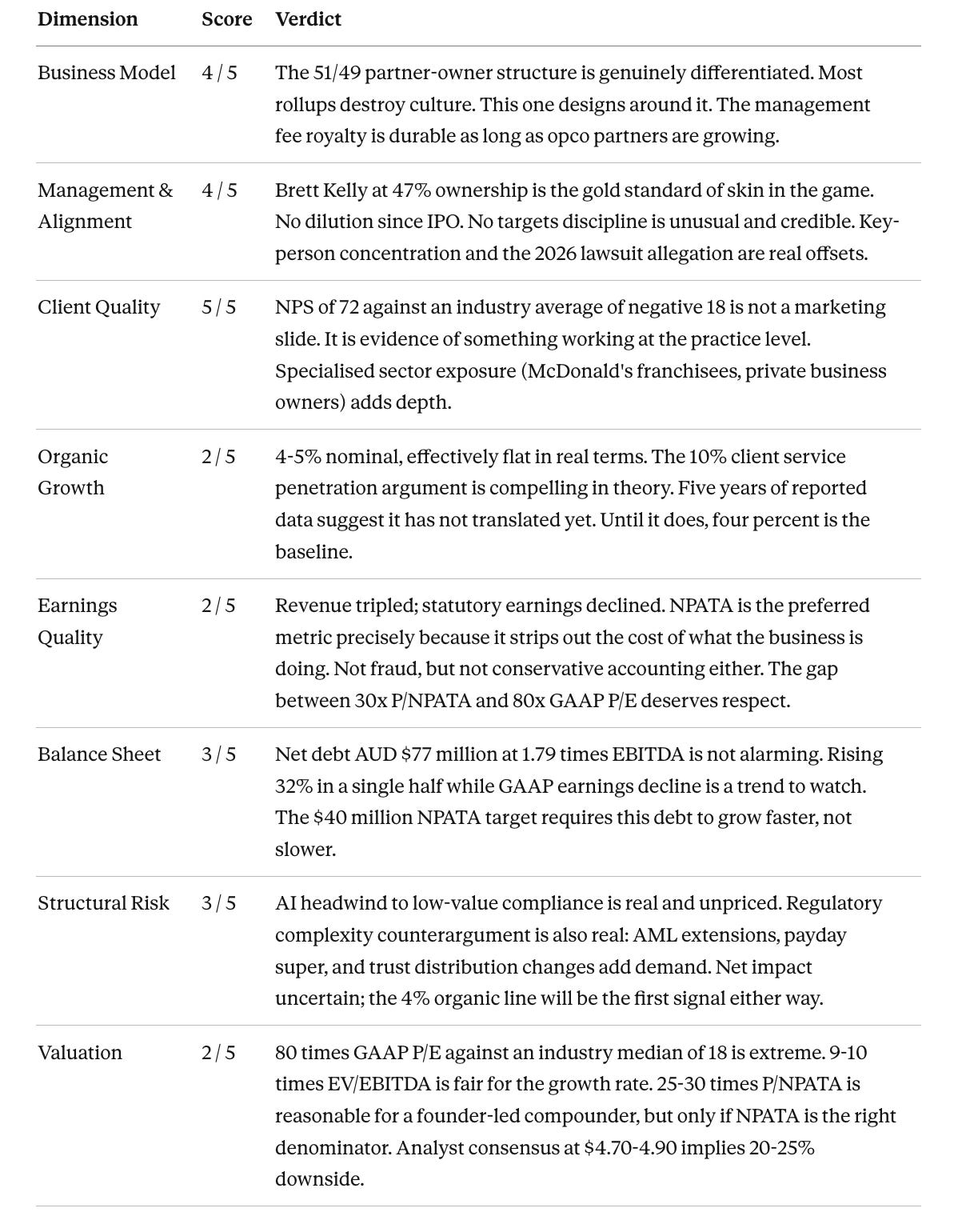

The Quality Scorecard

Eight dimensions. Each scored 1-5. The prose above justifies every number.

Overall: 25 / 40

A good business at a price that has been pricing a great one. The scorecard scores would improve meaningfully if organic growth accelerates or the US operation becomes clearly profitable. Neither has happened yet.

Building a Fair Value

Valuing Kelly Partners requires choosing your methodology carefully, because the metrics do not all point to the same place.

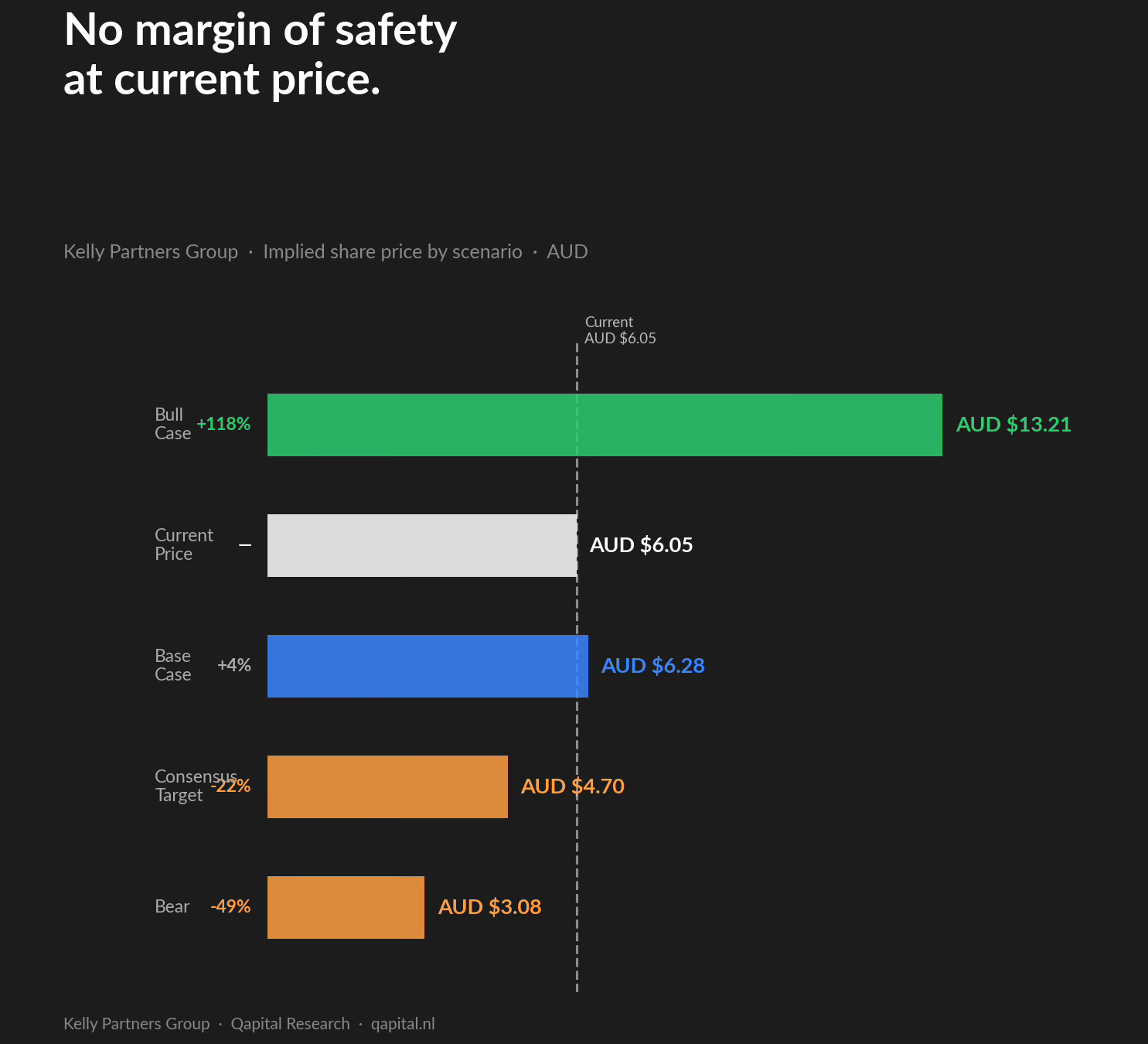

On GAAP P/E: At around AUD $6.00 per share and approximately 45.6 million shares outstanding, the market capitalisation is roughly AUD $274 million. FY2025 statutory earnings attributable to shareholders were AUD $3.41 million. That is a trailing P/E of approximately 80 times, compared to the Global Professional Services industry median of around 18 times. On this basis, the stock is pricing in a dramatic earnings recovery that the recent trend does not support.

On EV/EBITDA: Enterprise value (approximately AUD $274M equity plus AUD $77M net debt) is around AUD $351 million. FY2025 underlying EBITDA was AUD $38-41 million depending on the measure used. That is approximately 9-10 times EV/EBITDA. For a professional services rollup with 17% total revenue growth, this is not obviously stretched. Private equity buyers typically pay 8-12 times for similar businesses. On this basis, the stock looks roughly fairly valued.

On P/NPATA: FY2025 underlying NPATA attributable to shareholders was AUD $9.1 million, implying approximately 30 times at current prices. Using the H1 FY2026 annualised run rate of approximately AUD $11.2 million brings that to around 25 times, which is not unreasonable for a founder-led business growing its preferred metric at 12-13%.

The management target test: The company’s internal plan calls for NPATA of AUD $40 million by 2031. At 25 times NPATA, that implies a market cap of AUD $1 billion, or roughly AUD $22 per share, a compelling return from current prices. But reaching $40 million requires approximately 28% annual NPATA growth from a base of $9 million. That kind of growth, with organic revenue at 4%, requires the acquisition machine to run at a pace and with a discipline that has not yet been demonstrated at scale. We think the $40 million target is a plan, not a forecast, and should be weighted accordingly.

The DayPriest test: One of the more rigorous independent analysts following KPG noted in January 2026 that at $8.40 the stock was pricing at 40-42 times NPATA, and explicitly declined to buy on the grounds that it was “perfection multiple pricing.” At $6.00 that multiple has compressed to around 25-30 times, which is more reasonable. But the same analyst’s core concern, that returns depend on the market maintaining a high multiple rather than the business compounding intrinsic value, applies at any price until organic growth improves.

If you believe NPATA is the right measure and 12-13% NPATA growth continues, a 20-25 times multiple implies fair value around AUD $5.00-6.25 per share. The stock is at the high end of this range.

If you believe the acquisition treadmill will eventually slow, organic growth will not improve meaningfully, and the AI headwind compresses acquisition multiples, then reverting toward GAAP earnings, or toward a more conservative EV/EBITDA of 7-8 times (our assumed fair-value band for a slower-growth scenario), implies fair value closer to AUD $3.50-4.70. Analyst consensus targets cluster in the AUD $4.70-4.90 range, which falls precisely here.

The stock has continued falling since early 2026, declining from around $8.40 in January to around $6.00 today. That is a 29% decline in two months, suggesting the market is actively repricing the narrative, not finding a floor.

The Bold Call

Brett Kelly has built something real. The partner-owner model is genuinely differentiated from most accounting rollups. The alignment structure is thoughtful. The NPS of 72 against an industry average of negative 18 is evidence of authentic service quality. The Australian operation is profitable and cash-generative. The management team does not dilute shareholders, does not rush acquisitions, and does not set targets that pressure bad decisions. Calling Kelly Partners a fraud or a house of cards would be wrong.

But the micro-cap newsletter industry has attached a compounder premium to a business whose statutory earnings have declined on a five-year view. The preferred metric, NPATA, strips out the very cost that makes the rollup engine run. The organic growth is four percent. The management’s own $40 million NPATA target implies a 28% annual growth rate that has never been demonstrated and requires the acquisition treadmill to accelerate dramatically. The AI disruption to compliance volume is a real and unpriced risk. The US expansion is unproven. The stock is in an accelerating downtrend.

The stock at AUD $13.60 was pricing in a decade of flawless execution and multiple expansion. The stock at AUD $6.00 is pricing in continued execution with more measured expectations. Neither is obviously a bargain.

Analyst consensus targets cluster around AUD $4.70-4.90, implying meaningful downside from current levels. We think that range is more likely to prove correct than the prevailing newsletter narrative. On a fair-value basis, applying our assumed 8 times EV/EBITDA to current earnings and accounting for rising debt, we arrive at an intrinsic range of AUD $4.50-5.50 per share.

Our rating: CAUTIOUS. The business deserves respect. The narrative deserves scrutiny. The price deserves patience. Kelly Partners at AUD $4.50, if the organic growth story stabilises, the US finds its footing, and the $40 million NPATA target starts to look credible, is a genuinely interesting conversation. At AUD $6.00 with statutory earnings declining, debt rising, the acquisition treadmill accelerating, and the stock in a downtrend, the risk-reward is not compelling.

The paid platforms told you this was a compounder. The earnings said otherwise. Trust the earnings.

This article is for informational purposes only and does not constitute investment advice. All figures in AUD unless noted. Prices and targets as at March 2026.