GigaCloud Technology: The cheapest quality business you passed because of its passport

Ticker: NASDAQ: GCT Current Price: Around USD $44 (as at March 2026) 52-Week Range: USD $12.47 to $52.88 Qapital Rating: CAUTIOUS BUY

The discount nobody earned

Here is a question worth sitting with. A business generates $1.29 billion in revenue. It holds $417 million in total liquidity. It carries zero debt. It grew its active buyer count by 30% last year. It generated $191 million in operating cash flow. It just turned a bankrupt acquisition profitable in under two years, ahead of its own schedule. It topped Forbes’ annual list of the most successful small-cap companies in 2024. It was included in the Russell 2000 in 2024. Its founder won EY Entrepreneur of the Year for Greater Los Angeles. The auditor is KPMG.

What multiple does it trade at?

Ten times earnings. Against a peer average of 32.7 times.

If this were a Boston-based SaaS company, it would be on the cover of every growth newsletter in the country. It is not a Boston-based SaaS company. It is a Los Angeles-based B2B marketplace founded by a Chinese-American entrepreneur, and it has been the subject of two short-seller reports in the past three years.

That is the entire explanation for the discount. Not the fundamentals. Not the cash flow. The passport.

The Behavioral Lens: Guilt by association

The investment community has a well-earned scar from Chinese-founded, US-listed small caps. Luckin Coffee fabricated transactions. Uxin inflated used car sales. A generation of small-cap frauds taught investors a pattern-matching heuristic: Chinese-founded, US-listed, short-seller report equals fraud, sell, move on.

The heuristic is useful on average. Applied without discrimination, it creates exactly the kind of mispricing that careful investors are paid to exploit.

Psychologists call this availability bias. The most vivid examples, Luckin and its peers, are most easily recalled, so they dominate the mental model. The result is that investors apply a fraud discount to every company that resembles the template, regardless of whether the underlying facts support it. GigaCloud fits the template in surface features. It does not fit it in substance.

Two short-seller reports have now been answered. The first, from Culper Research in September 2023, was formally investigated by an independent forensic team: White and Case as legal counsel and FTI Consulting as forensic accountants. The Audit Committee concluded the allegations were not substantiated. KPMG continued providing unqualified audit opinions. The second, from Grizzly Research in May 2024, alleged related-party shell companies inflating marketplace metrics. GigaCloud denied the claims, citing SEC disclosure compliance. KPMG signed again. The cash kept accumulating.

Neither report produced a restatement, a regulatory action, or an auditor resignation. What they produced was a multiple stuck at ten times earnings.

The question is not whether the short sellers were malicious. The question is whether the discount they created is warranted by the evidence that now exists. It is not.

The Machine: What GigaCloud actually does

Most coverage of GigaCloud calls it a B2B marketplace. That is accurate but incomplete. Understanding why it is genuinely hard to replicate requires understanding the whole system.

GigaCloud connects Asian manufacturers, primarily in China and increasingly in Southeast Asia, with resellers across the United States, Europe, and Japan. The product category is large-parcel goods: furniture, appliances, fitness equipment. These are the items that nobody else wants to ship. A sofa is not a t-shirt. It requires different ocean freight containers, different warehouse infrastructure, different last-mile delivery networks, and different damage claim processes.

GigaCloud built all of it. The company operates its own warehousing network in the United States and Europe, manages ocean freight logistics, and handles last-mile delivery for oversized items. This is the moat the short-seller reports missed: even if you could replicate the marketplace technology, replicating the physical logistics infrastructure takes years and hundreds of millions of dollars.

The business model has two sides. The first-party (1P) business involves GigaCloud buying inventory directly and reselling it. The third-party (3P) business earns fees from facilitating transactions between independent sellers and buyers. The transition toward 3P is the most important structural trend in the business: 3P now represents 54% of total marketplace GMV, and in the United States specifically, 73% of GMV came from 3P transactions in Q4 2025, up from just 49% in Q1 2022. This is the same transition Amazon and Alibaba made, from retailer to platform. Europe is still predominantly 1P at 89% of GMV, which means the 3P conversion opportunity there is largely untapped.

The company calls its model SFR: Supplier Fulfilled Retailing. The manufacturer ships directly from their facility to the buyer, with GigaCloud handling logistics coordination. This eliminates the double-handling cost that traditional wholesale distribution creates. It is not a marketing label. It is a genuine cost advantage that explains why sellers and buyers choose the platform despite alternatives.

The M & A Proof of Concept

The most underappreciated part of the GigaCloud story is what happened after the Noble House acquisition in 2023. GigaCloud acquired Noble House, a furniture brand that had filed for bankruptcy, at a point when the business was losing approximately $40 million per year. The original target for returning Noble House to profitability was Q2 2026. GigaCloud reached that milestone in Q4 2025, at least two quarters ahead of schedule.

This matters for two reasons. First, it demonstrates that GigaCloud’s operational playbook can absorb a distressed asset and fix it. The logistics infrastructure, supplier relationships, and marketplace distribution that felt like theoretical moats have been tested under real conditions and worked. Second, it answers the implicit governance question better than any forensic report: a company that is fabricating transactions does not simultaneously run a successful turnaround of a bankrupt acquisition.

In January 2026, GigaCloud announced the acquisition of New Classic Furniture for $18 million in cash. New Classic focuses on brick-and-mortar distribution, a channel GigaCloud has historically underserved. Management has laid out a six-quarter integration plan that mirrors the Noble House approach. The mid-teens million dollar revenue contribution expected in Q1 2026 alone suggests the asset was not bought at a premium.

Europe as the Next Frontier

Europe grew revenue 66% in full-year 2025. GigaCloud now operates seven warehouse facilities across the continent, with Germany as the original beachhead and expansion accelerating. Europe has become the company’s strongest-growing region. The structure there differs from the US: 89% of European GMV is currently 1P, which means the margin profile is lower, but it also means that as 3P penetration grows in Europe, the unit economics will improve materially over time. The international build-out requires capital and patience. The Q4 2025 numbers suggest the capital is being deployed well.

The numbers that do not lie

FY2025 results were filed in February 2026, and they are not ambiguous.

Revenue reached $1,289.9 million, up 11.1% year-on-year. That number understates the platform’s momentum because revenue growth in the 1P business can decelerate while the marketplace itself accelerates: GMV reached $1,576.8 million, up 17.5%. The 3P business, which contributes less to reported revenue per dollar of GMV but more to margin, grew 23%.

Active buyers grew 29.9% to 12,089. Active third-party sellers grew 16.9% to 1,299. Average spend per active buyer held at approximately $130,000 annually. That figure matters because it is a proxy for buyer dependency: a reseller spending $130,000 per year through a single platform has built their supply chain around it. Switching cost is real. The cohort data reinforces this: buyers who joined the platform in 2024 grew their quarterly spend from $86 million to $99 million in a single quarter.

Net income was $137.4 million, up 9.2%. Diluted EPS was $3.59. Operating cash flow for the full year was $191 million. Total liquidity at year-end, including cash, restricted cash, and short-term investments, was $417 million. Debt was zero.

One number deserves honest acknowledgment. US product revenue grew only 3% year-on-year. The overall growth picture looks stronger because of Europe and the 3P mix shift. But the US core business, which remains the largest segment, is not compounding fast in 2025. This is likely a combination of tariff-driven inventory caution among buyers and broader softness in the large-parcel home goods category. Management is addressing it through supply chain diversification and new buyer acquisition. The trajectory, not the absolute rate, is what matters here.

In Q4 2025 specifically: revenue reached $363 million, up 22.7%. Gross profit was $83 million at a 28% margin. Net income was $39 million with an 11% net margin. Diluted EPS reached $1.04, up 40%. The most recent quarter is the strongest quarter in the company’s history. The stock rose 33% on earnings day and is still at ten times trailing earnings.

Q1 2026 guidance: $330 to $355 million in revenue, which includes mid-teens million dollar contribution from New Classic. Annualised, that puts the forward run rate at $1.3 to $1.4 billion.

The Short Seller Question

The honest treatment of both reports requires separating what was investigated and cleared from what remains formally open.

The Culper Research report (September 2023) alleged that GigaCloud’s warehouse operations could not be supported by disclosed headcount, and raised questions about the cash balance. GigaCloud engaged White and Case and FTI Consulting for an independent forensic review. The Audit Committee concluded the allegations were not substantiated. KPMG maintained its unqualified audit opinion throughout. That matter is effectively closed.

The Grizzly Research report (May 2024) is more pointed. It alleged that GigaCloud operated a network of undisclosed related-party shell companies that transacted with the marketplace to inflate buyer count and GMV metrics. Import data, Grizzly claimed, showed that more than half of shipments were going to entities that appeared to be related parties or shells. GigaCloud’s response was a denial, asserting that all related-party transactions required by SEC rules had been disclosed.

Here is what makes this harder to dismiss than the Culper report: Grizzly’s methodology was based on external data, customs import records, which is verifiable in ways that a denial does not definitively counter. There has been no independent forensic review commissioned specifically addressing the Grizzly allegations. No regulatory action has followed. KPMG has continued to sign. But the formal resolution that the Culper report received has not been applied to the Grizzly allegations.

The Noble House turnaround provides circumstantial evidence that the business is real. A company running a fabrication scheme does not simultaneously execute a complex operational turnaround of a bankrupt acquisition, ahead of schedule, in a different product category. The $191 million in operating cash flow for 2025 is difficult to fabricate across multiple audit cycles. But the Grizzly report cannot be categorically dismissed on available evidence, and any serious assessment of GigaCloud must acknowledge this as an open item rather than a resolved one.

If the Grizzly allegations were substantially correct, the discount is warranted. If they were not, the stock is one of the most mispriced businesses in US small-caps.

The Tariff Cloud

The legitimate operational risk for GigaCloud is not fraud. It is trade policy.

The company’s supply chain was historically concentrated in China. US tariffs on Chinese imports represent a direct cost headwind on every unit of inventory sourced, shipped, and warehoused. GigaCloud guided a 2.5% gross margin headwind from tariffs in Q3 2025. That is not trivial for a business running mid-to-high 20% gross margins.

The company is responding with supply chain diversification. Management has stated that more than 50% of the first-party supply chain supporting the US market now comes from Southeast Asia: Vietnam, Malaysia, and others. This shift reduces tariff exposure on Chinese goods but introduces a new set of complications: fewer established supplier relationships, different quality controls, and logistical routes that the company’s infrastructure was not originally optimised for. There is also a secondary risk that tariffs could expand to cover Southeast Asian goods, which would reduce the benefit of the geographic shift.

There is an additional layer of margin pressure that the tariff debate often obscures. Service revenue margins fell to approximately 6% in Q4 2025, down from 9% the prior quarter. Two forces drove this: holiday season shipping surcharges hit logistics costs, and ocean spot freight rates compressed after falling from elevated post-Liberation Day levels. Service margins at 6% are below where the business can sustainably operate. Management expects normalisation through 2026 as spot rates stabilise, but it is a variable that bears watching.

International revenue is growing faster than US revenue, with Europe now the strongest-growing region at 66% year-on-year. This geographic diversification reduces the tariff impact on the portfolio, but it also requires building the same logistics infrastructure in Europe that took years to build in the United States.

The tariff risk is not existential. GigaCloud is not a tariff story in the way that a company with 100% China sourcing and no pricing power would be. But margin compression in 2026 is a realistic scenario, and the Q1 2026 guidance of $330 to $355 million should be read against that backdrop.

The condition that would most rapidly change the risk profile is a material reduction in US tariffs on Southeast Asian goods. The condition that would most damage the thesis is an escalation to broad tariffs on all non-US manufactured goods combined with a failure of the supply chain diversification to hold margins.

The team

Larry Wu founded GigaCloud in 2006 and has served as Chairman and CEO since the beginning. He holds an MBA from Yale (2002) and a mechanical engineering degree from Beijing Union University. Before GigaCloud, he served as General Manager at New Oriental Education and Technology Group, one of the largest education companies in China and a legitimate NYSE-listed business. He was named EY Entrepreneur of the Year 2024 for Greater Los Angeles, a recognition not given to founders of fraudulent businesses.

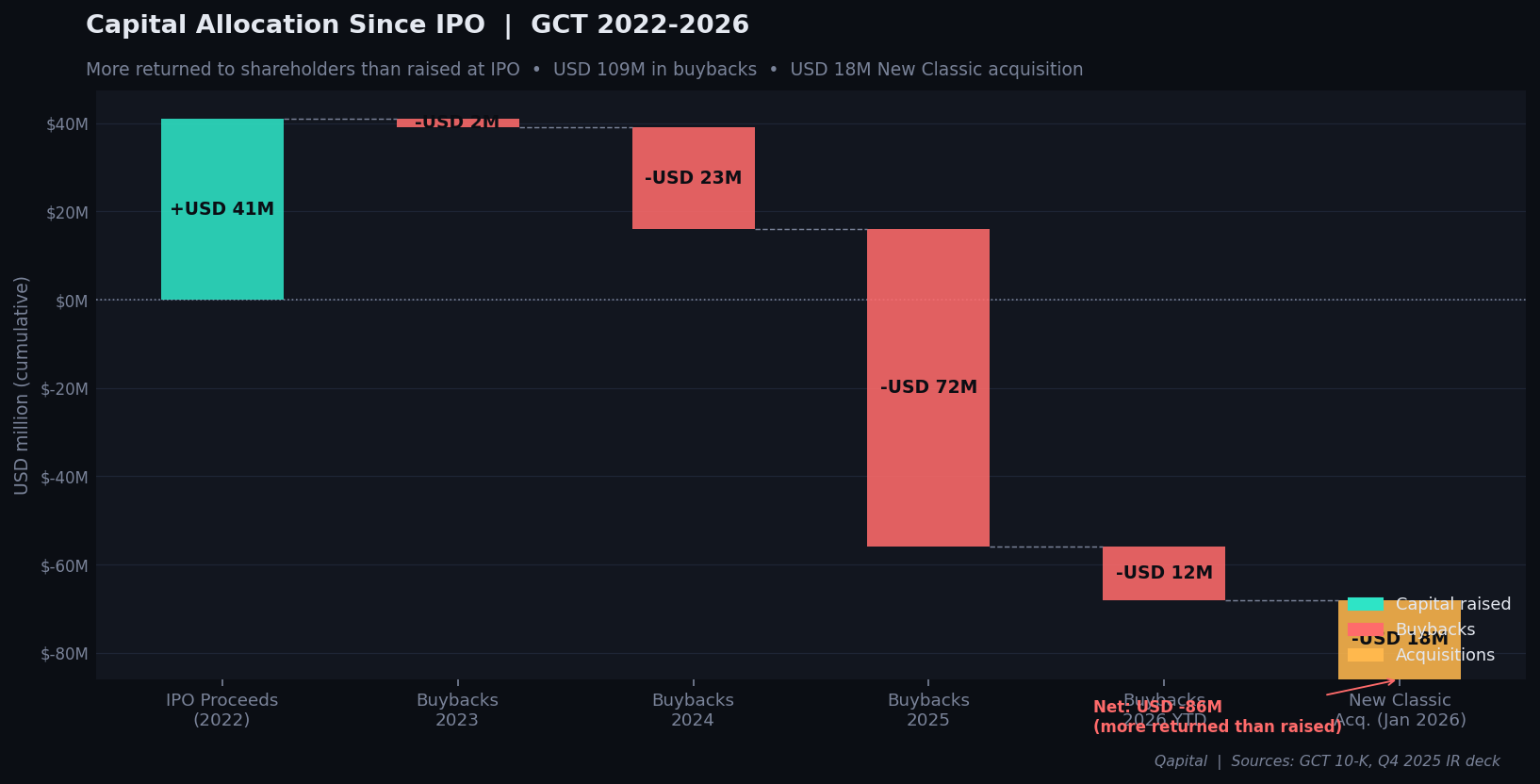

The capital allocation history tells a clear story. GigaCloud raised $41 million at its IPO in 2022. Since then, the company has bought back $109 million in shares and deployed $105 million in acquisitions (Noble House and New Classic). Management has returned more capital to shareholders than it raised at the IPO. The buyback programme is not a press release exercise: in 2025 alone, the company repurchased $72 million of stock. Through the first two months of 2026, another $12 million has been bought back. According to company disclosures, the weighted average repurchase price across the program is $31.60 per share, meaning management has been buying at approximately 28% below the current $44 price. That is the clearest signal available about where insiders believe intrinsic value sits.

The $111 million buyback authorisation announced alongside the Q4 2025 results extends the programme. At a market cap of approximately $1.6 billion with $417 million in total liquidity and zero debt, authorising a buyback worth roughly 7% of market cap is a statement. Management does not return capital at this pace unless it believes the stock is priced well below fair value.

The key-person risk is real: this is a founder-led business where the marketplace relationships, supplier network, and operational playbook are concentrated in a small team. What mitigates this partially is the physical infrastructure layer. The warehouses, logistics contracts, and freight relationships would survive a leadership transition in ways that a purely software-based platform would not.

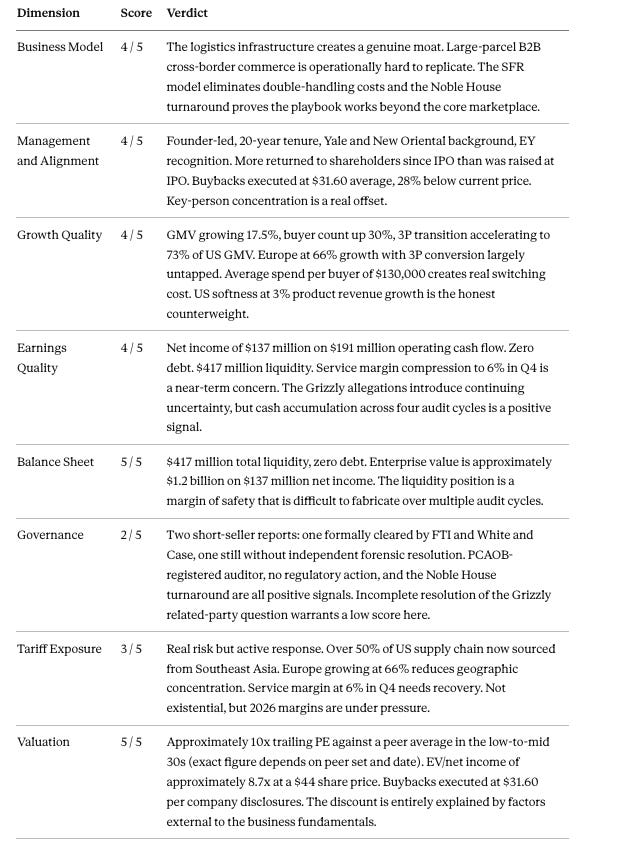

The Quality Scorecard

Eight dimensions. The research above justifies every score.

Overall: 31 / 40

A high-quality business with a governance question that the market has priced as a fraud discount. If the Grizzly allegations are unfounded, this score should be 35 or 36 out of 40 and the stock is significantly undervalued. The balance sheet strength and the buyback execution at prices well below current levels suggest the insiders believe it belongs there.

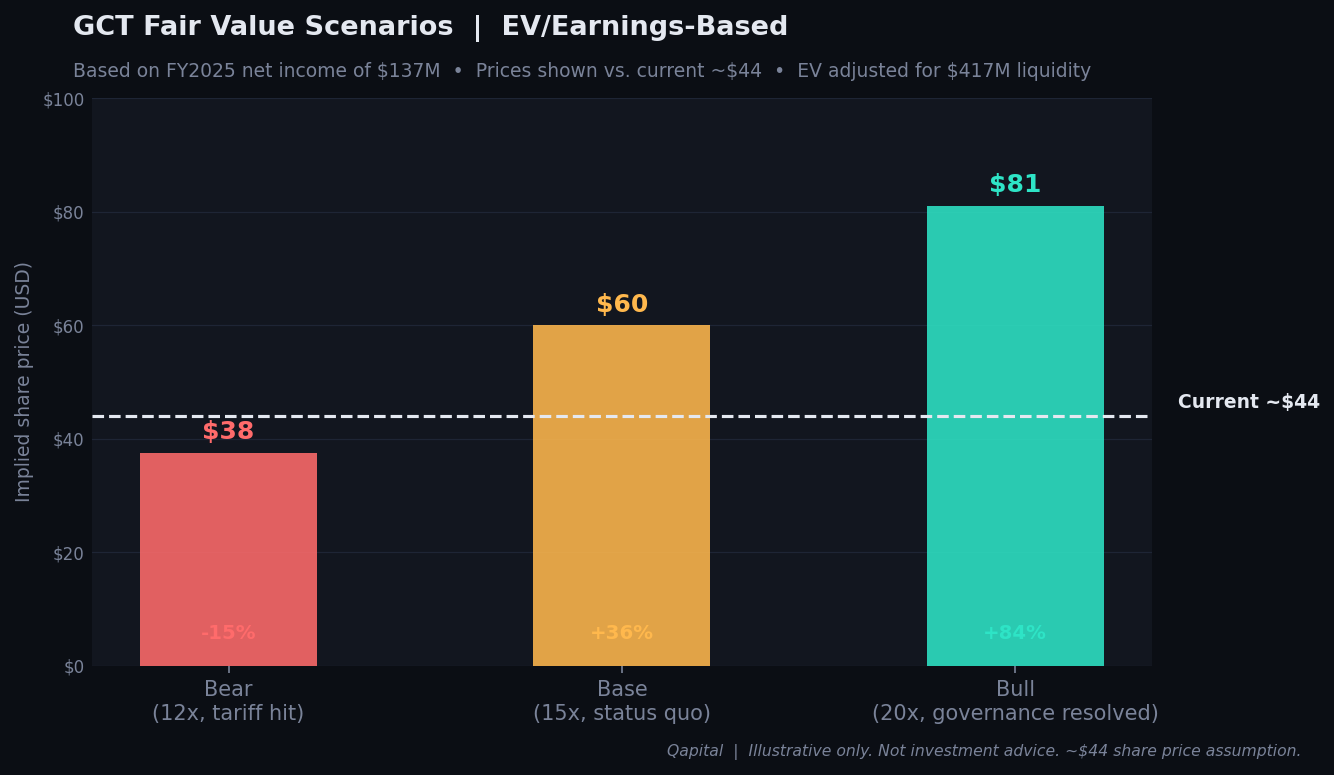

Building a fair value

The starting point is the liquidity. GigaCloud holds $417 million in total liquid assets with no debt. At a market cap of approximately $1.6 billion (based on a share price around $44 at time of writing), the enterprise value is roughly $1.2 billion. All valuation work below uses enterprise value, not market cap. These multiples move with the live price and should be updated accordingly.

On EV/Earnings: At around a $44 share price, total liquidity of $417 million, and zero debt, enterprise value is roughly $1.2 billion. FY2025 net income of $137.4 million against that EV gives an EV/net income ratio of approximately 8.7 times. Peer average is 32.7 times. The implied fair value at a 20 times EV/earnings multiple, which is well below peers and appropriately conservative given governance uncertainty, is approximately $81 per share. At 15 times, the implied price is approximately $63. Both represent significant upside from the current $44.

On Forward Earnings: Q1 2026 guidance of $330 to $355 million in revenue, if maintained across the year, implies annual revenue of approximately $1.3 to $1.4 billion. With stable margins, forward net income could reach $140 to $150 million. At a forward PE of 12 times (still a steep discount to peers), that implies a stock price of approximately $46 to $50, close to current levels. At 15 times forward earnings, $58 to $62.

The tariff scenario: If tariffs compress gross margins by a further 2 to 3 percentage points through 2026, and management cannot fully offset through pricing or supply chain savings, net income could decline toward $110 to $120 million. At 12 times that range, fair value falls to approximately $35 to $40, below the current price. This is the bear case. Note that with $417 million in liquid assets, the downside is partially cushioned.

The governance resolution scenario: If GigaCloud were to commission and publish an independent forensic review specifically addressing the Grizzly allegations, and that review cleared the claims as the Culper review did, the governance discount would have no remaining factual basis. A re-rating toward 20 times earnings, which would still represent a discount to peers, implies a stock price above $80.

The base case, no governance resolution but continued operational execution and modest tariff headwinds, suggests fair value in the $55 to $65 range over 12 months, representing 25 to 50% upside from current levels.

The Bold Call

GigaCloud is not a fraud story. The cash is real. The buyers are real. The warehouses exist across two continents. The Noble House acquisition, bought in bankruptcy, was turned profitable ahead of schedule. KPMG has signed four consecutive unqualified opinions since the first short-seller report. Larry Wu is spending more of the company’s cash buying back stock than he raised at the IPO. That is not the behaviour of a man who believes the fundamentals are fabricated.

The Grizzly Research allegations are the one legitimate reason for caution. They have not been definitively cleared with the same rigour as the Culper report, and intellectual honesty requires stating that plainly. An investor who demands complete governance resolution before buying should wait. An investor comfortable holding the governance question alongside $417 million in liquidity, zero debt, 30% buyer growth, and a 10x earnings multiple has a genuinely asymmetric setup.

The market has applied the Chinese fraud heuristic to a business that has, on every available measure of substance, continued to compound value. Availability bias created the discount. Continued operational execution will eventually close it.

The tariff risk is real and the 2026 numbers may disappoint on margins. We have been explicit about this. If supply chain diversification stalls and margin compression accelerates, the bear case is $35 to $40 per share. That is the downside with $417 million in liquid assets as your floor.

The upside, at a modest but still discounted 20 times earnings on current numbers, is above $80.

Our rating: CAUTIOUS BUY. The caution is the governance note. The buy is everything else. At $44 with $417 million in liquidity and zero debt, you are being paid to hold the uncertainty.

The market punished GigaCloud for looking like a fraud. It has not rewarded it for not being one. That gap is the trade.

This article is for informational purposes only and does not constitute investment advice. All figures in USD unless noted. Prices and targets as at March 2026.