Games Workshop: The most profitable hobby in the world

How a Nottingham plastics manufacturer generates 191% returns on capital and what that multiple is actually pricing in

The business: Miniatures, lore and cultural capital

Games Workshop makes highly detailed plastic and resin miniature figures, primarily in the Warhammer 40,000 and Warhammer: Age of Sigmar universes. The hobbyist community’s affectionate term for the product is ‘plastic crack.’ The joke captures something real: the hobby is highly adhesive, built on sunk creative investment, and almost impossible to leave once started. But it should not distract from the fact that this is a serious business with serious economics.

The company sells through three channels: a global network of independent trade retailers (approximately 8,600 accounts), 575 company-owned single-brand stores, and its own online webstore. A strategically important licensing segment generates royalty income from third parties using the Warhammer intellectual property, covering video games, board games, novels, animations and, increasingly, television.

Games Workshop was founded in Nottingham in 1975, originally as a publisher and distributor of American tabletop role-playing games. It developed its own wargaming system in the 1980s, launched Warhammer Fantasy Battle, then Warhammer 40,000 in 1987. Today it operates from a campus in Lenton, Nottingham, employs around 3,600 people in 25 countries, and distributes to 58 export territories globally.

The revenue model is deceptively simple: design miniatures, manufacture them in-house, sell them. There is no subscription, no platform fee, and no lock-in mechanism beyond the one the hobby creates organically. The average hobbyist spends years in the category, painting, collecting, playing and building armies, and each army, once started, pulls you deeper. New editions, new factions, new campaigns. The content refresh cycle keeps customers spending continuously across a hobby lifetime measured in decades.

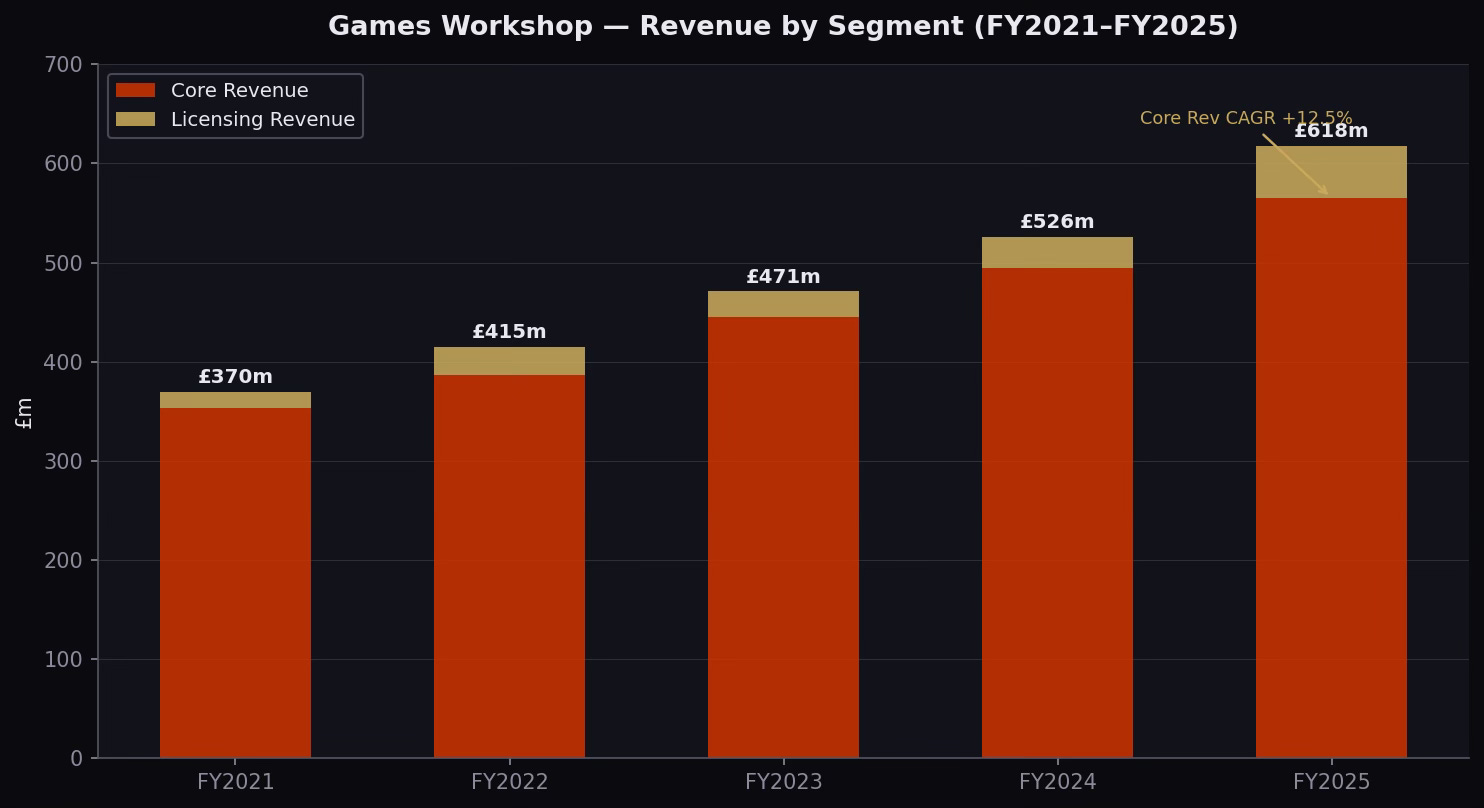

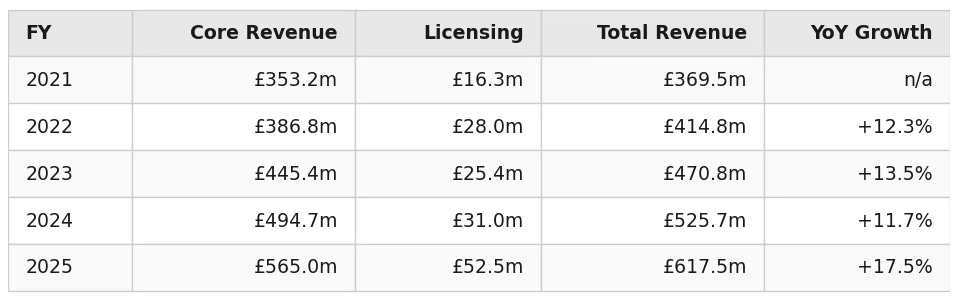

Revenue in FY2025 (52 weeks ended 1 June 2025) totalled 617.5m GBP, of which 565.0m GBP was core product revenue and 52.5m GBP was licensing. North America is the single largest geographic market at 44% of core revenue (249.3m GBP), followed by Continental Europe (25%, 140.8m GBP), the UK (21%, 117.9m GBP), and a growing Asia/ANZ segment.

What makes this business tick: The moat

A 191% ROCE is not an accident. It is the financial output of a moat structure that is unusually wide and unusually durable. There are five layers worth understanding.

Layer 1: Forty years of world-building

Warhammer 40,000 is one of the most elaborately developed fictional universes in existence. It spans tens of thousands of pages of novels, hundreds of video games, decades of miniature releases, and a creative community of millions. The depth of the lore creates genuine switching costs: a hobbyist invests not just money but imagination and identity into this world. Leaving is not like cancelling a streaming subscription. The Black Library (Games Workshop’s publishing arm) sells novels set in this universe. The Warhammer+ streaming service has grown to 248,000 subscribers. The lore machine compounds.

Layer 2: The community as network effect

Unlike most consumer goods categories, Warhammer generates community as a by-product of consumption. Local gaming clubs, Warhammer Alliance school programmes (6,600 active clubs globally), the Warhammer Community website, and the global events programme (15 major events in H1 FY2026 alone, reaching nearly one million attendees) create a social infrastructure that reinforces the habit. New hobbyists join through friends, clubs and stores. The hobby recruits itself.

Layer 3: Customer acquisition embedded in retail

Games Workshop’s 575 single-brand stores are not profit centres in the traditional retail sense. They are customer acquisition assets. Staff are trained to introduce new people to the hobby, offering free introductory experiences, teaching beginners how to build and paint, and running demo games. Around 424 of the 575 stores are single-staff, low-cost format (average new store fit-out: approximately 45,000 GBP), which makes the network economically viable even at modest revenue per store.

Layer 4: Vertical integration from IP to shelf

Games Workshop designs every miniature in its Warhammer Studio in Nottingham. It manufactures them in its own factories using injection moulding machines it tools itself, with proprietary moulds. It warehouses and distributes globally from Nottingham, Memphis and Sydney. Competitors cannot source comparable products from Games Workshop’s supply chain. The moat is structural, not contractual.

Layer 5: The collector psychology

This is the behavioural edge. Miniature hobbyists exhibit what behavioural finance might call sunk-cost reinforcement: the more armies you own, the more invested you are in the universe, and the more new releases pull you forward. Painting a miniature, which can take hours per model, creates an emotional attachment that no digital entertainment can replicate. The product is tangible, tactile, and deeply personal. Price increases of approximately 3.5% were introduced in H1 FY2026 in response to tariff pressures, with no material demand impact reported. This is a category without an adequate substitute.

Five-year financial performance

The numbers tell a consistent story: compounding, capital-light growth with expanding margins.

Revenue

Chart 1: Core and licensing revenue FY2021-FY2025. Core revenue CAGR +12.5%

Core revenue has grown at a 12.5% CAGR over five years, with no year of decline. The licensing surge in FY2025 (+69% to 52.5m GBP) was driven primarily by the extraordinary commercial success of Space Marine 2, launched in September 2024. The core business is the compounding engine; licensing is welcome upside, but it is also volatile and should be modelled separately.

Profitability

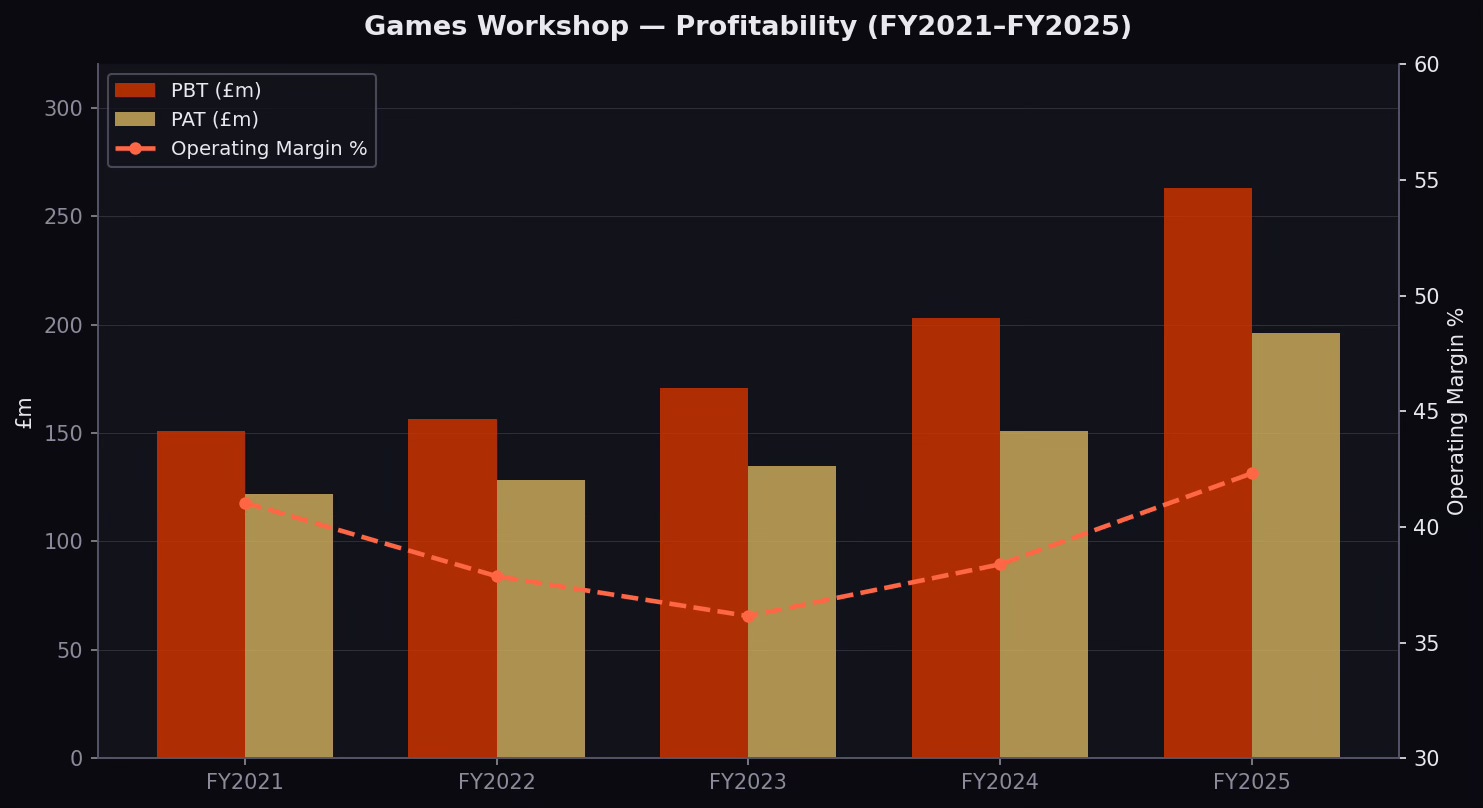

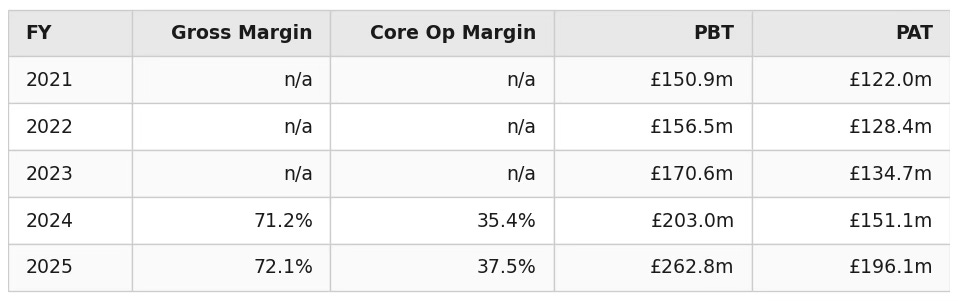

Chart 2: Pre-tax and post-tax profit (bars); operating margin % (line).

The 37.5% core operating margin in FY2025 is a five-year high, achieved on a cost base held largely stable relative to revenue. Operating expenses rose only 11.0m GBP year-on-year on a revenue increase of 91.8m GBP. Gross margin expansion (+90bps to 72.1%) reflects manufacturing efficiency gains, lower commodity costs and a favourable channel/product mix.

Keep reading with a 7-day free trial

Subscribe to Qapital to keep reading this post and get 7 days of free access to the full post archives.