Basic Fit: Europe’s largest gym sells intentions, not workouts

The low-cost fitness giant just turned the corner on free cash flow, acquired Europe’s largest franchise gym network, and is pivoting from aggressive growth to capital-light harvest. At €31, the market is still pricing in the fear. The fundamentals tell a different story.

The Behavioral Engine nobody talks about

Every January, millions of Europeans make the same resolution. They will start going to the gym. They sign up. They download the app. They go three times in February, twice in March, and then life gets in the way. But they keep paying.

This is not a failure of the fitness business model. It is the fitness business model.

Basic Fit has built one of the most psychologically durable recurring revenue streams in European consumer finance. Its members pay a fixed monthly subscription regardless of how often they visit. The average length of stay is 24 months. Churn is real but manageable, and the acquisition cost of a new member is low enough that the economics still work even if a significant portion of the base is what behavioural economists would call “optimistic non-attenders.”

Present bias is the tendency to overvalue immediate costs and undervalue future benefits. Most people, when signing a gym contract, genuinely intend to go. The friction of cancellation, combined with the nagging sense that they should start going again, keeps them subscribed far longer than their actual usage would justify. Basic Fit does not need to convince members to exercise more. It needs to convince them to stay subscribed while they are still intending to.

At €24.91 average monthly revenue per member in the owned club network, across 4.82 million Basic-Fit memberships within a total group base of 5.8 million, Basic Fit collects roughly €1.4 billion per year in subscription income from people who mostly believe they are about to become more active. The company’s job is simply to keep the clubs open and the brand relevant enough to prevent cancellation. At that price point, €24.91 per month, Basic Fit is also cheap enough that cancellation feels disproportionate to the friction involved. That is a competitive moat, and it compounds.

What Basic Fit actually does

Basic Fit is the largest fitness operator in Europe by club count, with 2,151 clubs across 12 countries as of December 2025. Of those, 1,716 are owned and operated clubs, and 435 are franchised under the Clever Fit brand following an acquisition in November 2025.

The business model is straightforward. Basic Fit builds or leases large-format fitness clubs in accessible locations, equips them with machines, and charges members a monthly subscription. There are no classes, no frills, and no personal trainers on staff. The model is deliberately stripped back to reduce operating cost, which allows the club to break even at relatively low membership density. Management estimates the break-even point at around 1,400 memberships per club. The average club in the owned network now carries 2,902 members. That gap between break-even and average capacity is where the economics get interesting.

Clubs are classified as mature once they have been open long enough to reach stable membership levels. In 2025, Basic Fit operated 1,216 mature clubs, and those clubs averaged an underlying EBITDA less rent of €369,000 per club per year, representing a return on invested capital of 31 percent. That is above the company’s stated 30 percent ROIC target, and it is a strong number for a business that builds its own clubs at an average cost of €1.33 million per opening.

The geographic split has shifted dramatically over the past three years. France is now the largest single market, generating €659.8 million in revenue in 2025. The growth segment of France, Spain, and Germany together accounted for 75 percent of revenue growth in 2025. France alone has 894 owned clubs, making it a dominant position in what is still a structurally underpenetrated European fitness market.

Germany tells a different story. Basic Fit had only 28 owned clubs in Germany at the end of 2024. Through organic openings and the Clever Fit acquisition, it ended 2025 with 44 owned Basic-Fit clubs plus 377 Clever Fit franchise clubs in Germany, making it the market leader in Europe’s largest consumer economy almost overnight.

The numbers behind the story

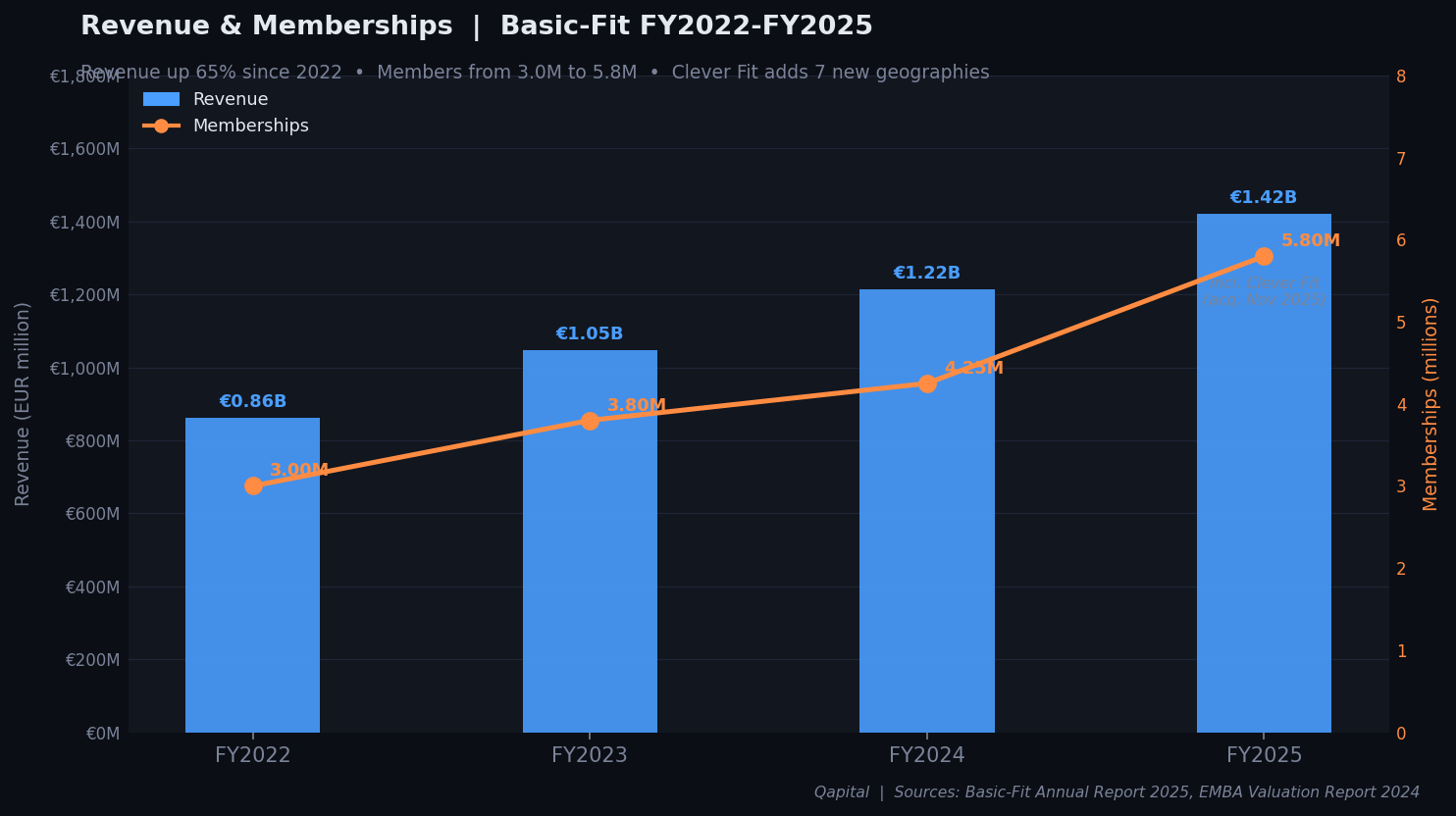

The 2025 full-year results represent the clearest inflection in Basic Fit’s financial history. Revenue grew 17 percent to €1,420.5 million. Club-level underlying EBITDA less rent, the measure that strips out corporate overhead, IFRS 16 lease accounting distortions, and exceptional items, reached €505 million for the owned club network. Group underlying EBITDA less rent, which deducts corporate costs, came in at €348.3 million, up 11 percent year on year. Excluding Clever Fit, the underlying group metric grew to €344.7 million.

The headline net profit of €14.3 million is misleading in isolation. The IFRS 16 lease accounting standard adds back a significant non-cash charge through right-of-use asset depreciation and interest on lease liabilities, which totals well over €300 million. The company’s own underlying net profit measure, which strips out IFRS 16 adjustments, PPA amortisation from acquisitions, and non-cash interest on the convertible bond, came in at €54.3 million, up 24 percent from €43.6 million in 2024.

The most important single data point in the 2025 report is free cash flow before acquisitions: positive €26.1 million. In 2024, the same line was negative €88.3 million. This swing of over €114 million reflects both the improving operating leverage of the club network and a deliberate slowdown in new club openings. Basic Fit opened a net 85 owned clubs in 2025, down from a faster pace in prior years, and the capital expenditure per new club remained controlled at €1.33 million.

Operating cash flow reached €647.4 million in 2025. After €411.4 million in investing activities, including the €139.3 million net cash outflow for the Clever Fit acquisition and €271.5 million in property, plant and equipment additions, and €177.7 million in financing activities including €29.4 million in share buybacks, cash on the balance sheet increased from €56.7 million to €115.0 million at year end.

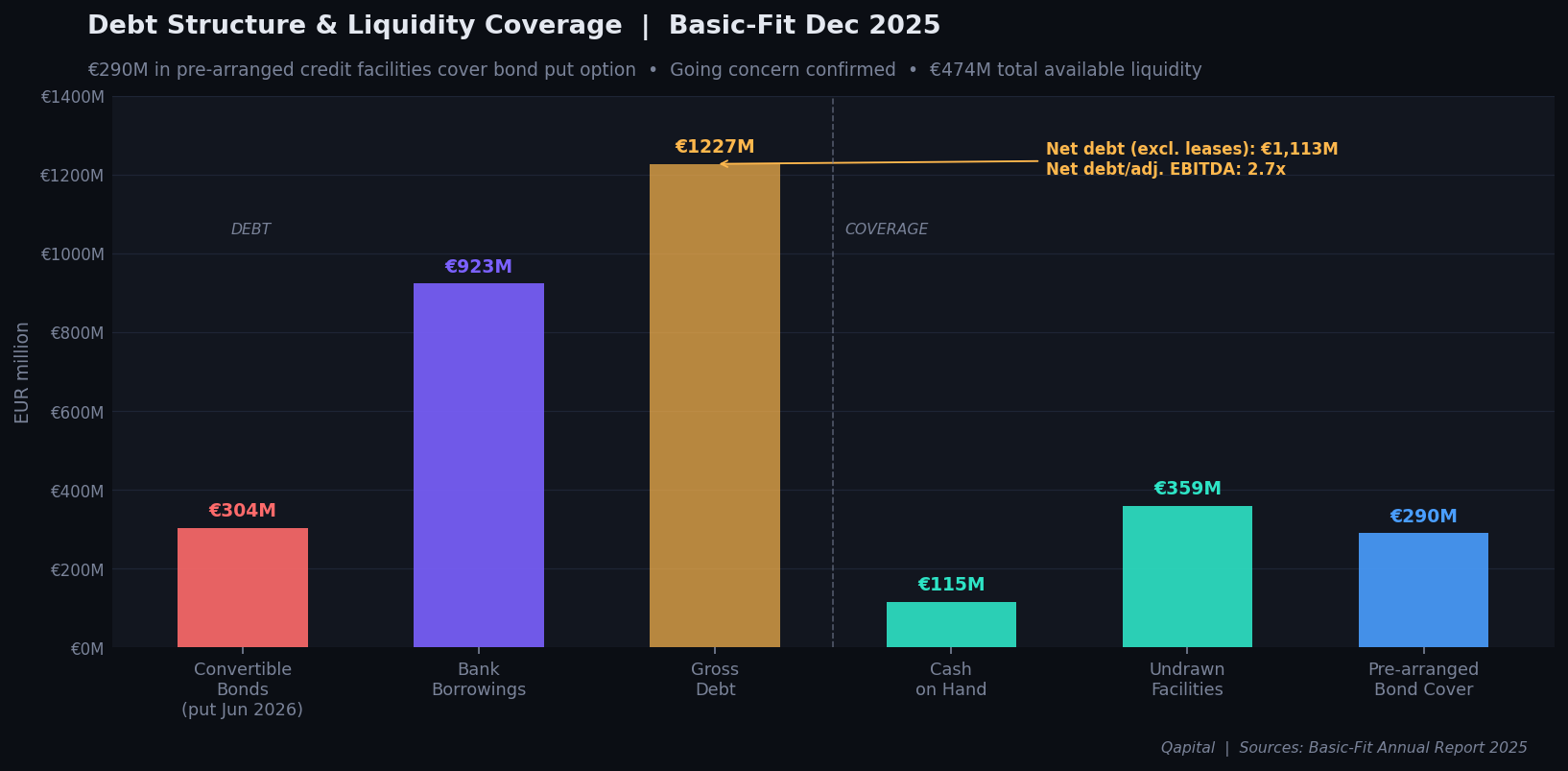

Net debt excluding lease liabilities stood at €1,113 million, representing a net debt to adjusted EBITDA ratio of 2.7 times. This is elevated but not alarming for an asset-heavy infrastructure business with contracted cash flows. The more pressing issue within the debt structure is examined in section 5.

The Clever Fit pivot: From builder to franchisor

The acquisition of Clever Fit in November 2025 for €160 million plus a €15 million earnout is the most strategically significant transaction in Basic Fit’s history, and the market does not yet appear to have fully priced it.

Clever Fit is Germany’s largest fitness franchisor, with 493 clubs at the time of acquisition across Germany, Austria, Switzerland, Slovenia, Romania, Croatia, and the Czech Republic. Of those clubs, 56 are company-owned and 435 operate as franchises, with franchisees paying a recurring fee of approximately 7 percent of revenue. Basic Fit paid roughly €160 million for a business that immediately made it the market leader in Germany, gave it seven new European geographies, and established it as the number one fitness franchisor on the continent.

The strategic logic runs deeper than the headline club count. Basic Fit has historically grown by building clubs it owns, leases for 10 to 15 years, and staffs. This is capital intensive. Each club costs €1.33 million to open and takes 12 to 18 months to reach break-even. The Clever Fit model is different. A franchisee builds and operates the club at their own capital expense. Basic Fit earns a royalty stream on revenue. The return on capital for a franchisor is structurally better than for an owner-operator.

This is why the 2026 strategic announcement matters. Basic Fit stated in January 2026 that it expects to limit new owned club openings to a net 50 in existing markets during 2026, compared to approximately 141 net new owned clubs in 2025. The shift in capital allocation is explicit. The company is de-emphasising owned club construction and emphasising franchise network growth, digital membership, and free cash flow generation.

The Capital Markets Day on April 21, 2026 is scheduled to provide a more detailed strategic update. Whatever management announces there will be the key catalyst for the next move in the stock.

The 56 owned Clever Fit clubs will be rebranded as Basic-Fit clubs during 2026, absorbing them into the core operating network. The franchise clubs will continue to operate under the Clever Fit brand. Basic Fit will begin layering in Basic-Fit franchise offerings in new markets, with Basic-Fit Franchise B.V. established specifically for this purpose. The long-term vision is a dual-brand franchise model across Europe: Basic-Fit in markets where the brand has equity, Clever Fit in Germany and adjacent markets.

The membership trajectory supports this ambition. In the first ten weeks of 2026, Basic Fit added more than 200,000 new memberships. The membership base closed 2025 at 5.8 million, up 36 percent year on year including the Clever Fit acquired members. Even stripping out Clever Fit, the Basic-Fit owned club membership base grew 13 percent to 4.82 million by end of Q4 2025. It is also worth noting that the franchise model is already generating tangible income: the two months of Clever Fit consolidation in 2025 contributed approximately €4.8 million in franchise fee revenue, a small but real taste of what a scaled royalty stream looks like.

The bond question, and why it just got simpler

Basic Fit has €303.7 million of senior unsecured convertible bonds outstanding, issued in June 2021 at a 1.5 percent coupon and maturing June 2028. For much of 2024 and early 2025 this was the dominant risk in every institutional conversation about the stock. As of March 2026, it is materially less of one.

The bonds carried a put option for bondholders exercisable in June 2026. By late 2025, management had assessed the likelihood of that put being exercised as high, pre-arranged €290 million in bilateral credit facilities with ABN AMRO, ING, and Rabobank to cover redemption requests, and recognised a €16.6 million non-cash catch-up charge in the 2025 income statement. Then, on March 3, 2026, Basic Fit announced it had paid bondholders a waiver fee of €2.75 million to neutralise the put option entirely. The June 2026 liquidity cliff is therefore off the table.

The residual question is the 2028 maturity itself. When the bonds come due in June 2028, Basic Fit will need to refinance €304 million at prevailing market rates. The current coupon is 1.5 percent, or roughly €4.6 million per year. A refinancing at around 4.5 percent would cost approximately €13.7 million per year, adding a net €9 million in annual cash interest. That is a real and permanent increase in the cost of debt, but it is manageable against €647 million in annual operating cash flow.

The conversion option on the bonds is out of the money at the current share price. The conversion price was set at a premium to the June 2021 stock price, meaningfully above €31. Equity dilution is therefore not a near-term concern unless the stock re-rates strongly above that level.

The financial accounting impact from the 2025 reassessment will actually produce a tailwind in coming years: the non-cash catch-up reverses, generating €4.1 million of benefit to reported finance costs in 2026, €8.5 million in 2027, and €4.0 million in 2028. The bond story has moved from “binary near-term event” to “manageable medium-term refinancing at a known cost premium.” That is a meaningful de-risking of the investment case.

Valuation: What the market is pricing in

Basic Fit trades at approximately €31 per share as of mid-March 2026, implying a market capitalisation of roughly €2.04 billion and an enterprise value of approximately €3.15 billion when net debt excluding lease liabilities is included.

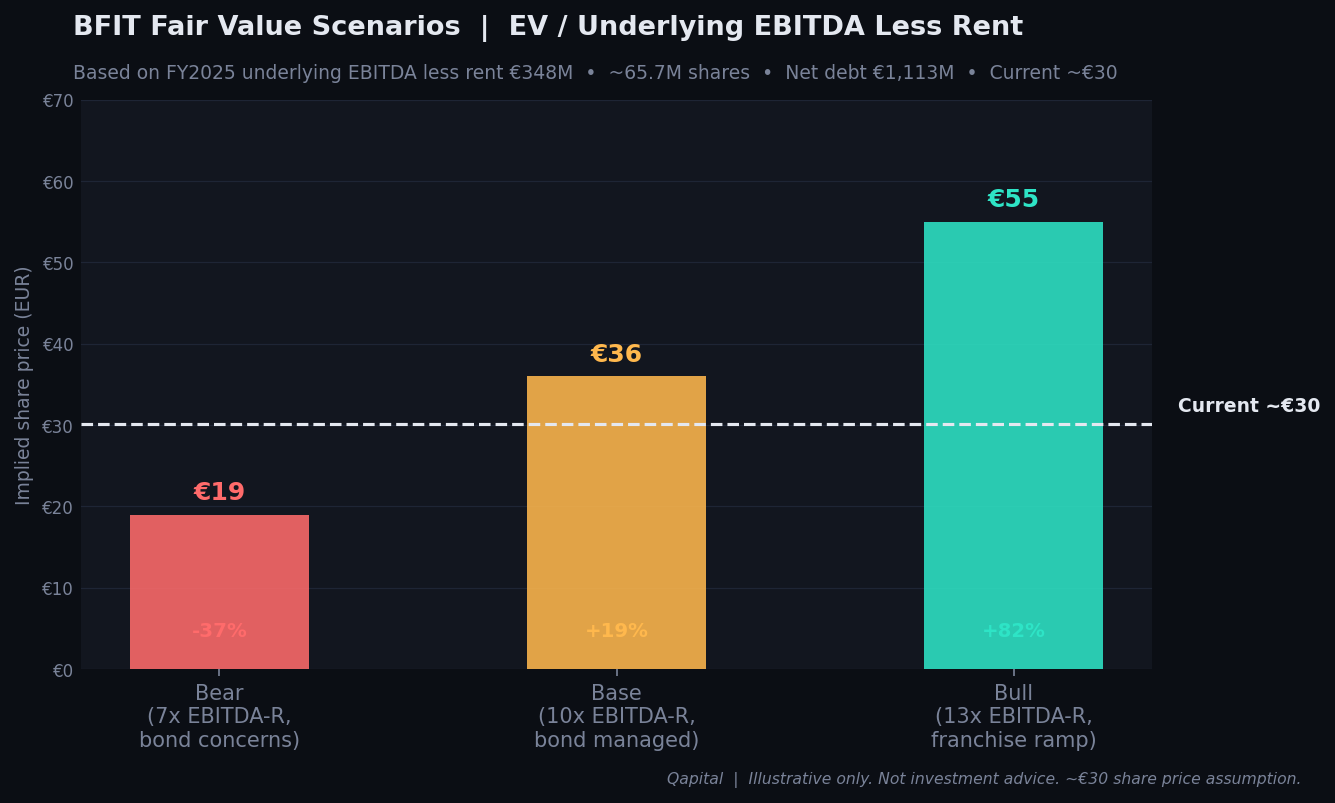

The appropriate valuation metric for a lease-heavy business like Basic Fit is enterprise value relative to underlying EBITDA less rent, which strips out both the IFRS 16 distortion and corporate exceptional items to reflect the true cash-generating capacity of the club estate. On this metric, Basic Fit trades at approximately 9.1 times the 2025 figure of €348.3 million.

That multiple looks optically cheap for a European consumer infrastructure business with a 31 percent ROIC on its mature club base. For context, comparable operators in European leisure and fitness typically trade at low-double-digit EV multiples when growth and FCF are both credible. Basic Fit’s discount reflects two persistent concerns: leverage and the convertible bond. Both are now more addressable than at any point in the past two years.

The analyst consensus on BFIT is a buy, with the average 12-month price target in the low-to-mid thirties. The range across analysts spans from the low twenties to the low forties, reflecting differing views on leverage and the pace of the franchise ramp rather than genuine disagreement about business quality.

The franchise pivot is worth dwelling on from a valuation perspective. An owner-operator that builds clubs with €1.33 million in capex per opening and a 12 to 18 month payback is a capital-intensive compounder — good, but slow. A franchisor that collects royalties on clubs built with someone else's capital is a structurally different business: lower near-term revenue growth, but higher return on incremental capital and faster FCF conversion. The terminal value of a franchise-heavy model should, in theory, be higher on a per-share basis than a pure owner-operator at the same revenue run rate. The market has not yet assigned that premium to Basic Fit, partly because the franchise contribution is still nascent. That gap is part of the opportunity.

If underlying EBITDA less rent reaches €380 to €400 million by year-end 2026, as the company’s own revenue and margin commentary suggests is plausible, and if the bond refinancing is executed cleanly, then at 10 to 11 times that figure the EV would be €3.8 to €4.4 billion. Against net debt of approximately €900 million to €1.0 billion (after FCF generation and bond refinancing), equity value would be €2.8 to €3.4 billion, or roughly €43 to €52 per share. The Capital Markets Day on April 21 is the likely moment when the market reassesses whether that narrative is credible.

The Bull Case: Harvest mode unlocks value

The single most underappreciated aspect of Basic Fit’s current position is what happens to the economics of a gym network when it stops building and starts harvesting.

For the past five years, Basic Fit has invested heavily in club construction, opening well over 100 clubs per year and accepting years of negative FCF in exchange for a larger installed base. The logic was sound: a mature club with 2,900 members generates a 31 percent ROIC at a capital cost of €1.33 million. Build enough clubs and the aggregate cash flow becomes enormous.

The pivot announced for 2026 suggests that management believes it has now built enough clubs in its core markets. By limiting openings to 50 and directing capital toward franchise expansion instead, Basic Fit should see a step-change in free cash flow. Maintenance capex runs at approximately €60,000 per club per year, meaning a stable network of 1,716 owned clubs costs roughly €103 million per year to maintain. Operating cash flow is €647 million. The gap between those two numbers is very large.

The franchise model compounds the opportunity. Each Clever Fit franchise club generates recurring royalty income for Basic Fit without requiring capital investment or lease obligations. As the franchise network grows, the cash flow quality of the overall business improves, because franchise income is higher margin and requires no reinvestment. If Basic Fit can add 50 to 100 franchise clubs per year from the Clever Fit and Basic-Fit Franchise platforms combined, it adds recurring income while keeping capex near maintenance levels.

The yield improvement story also has legs. Average revenue per member per month grew from €24.24 to €24.91 in 2025, driven by the rollout of tiered Premium and Ultimate membership options. Management stated that approximately half of all new joiners are now opting into the higher-priced tiers, and yield improvement is expected to continue into 2026. A move from €24.91 to €26 per member per month across 5.0 million owned-club members adds roughly €66 million to annual revenue with near-zero incremental cost. That flows almost entirely to EBITDA.

The stock has recovered sharply from its 52-week low of €16.50 and now trades at €31, still below the 52-week high of €34.40 and at a discount to the analyst consensus target of €34.19. The combination of operational momentum, FCF inflection, and a known catalyst in the April 21 Capital Markets Day makes the near-term setup constructive.

The Bear Case: Leverage, bonds and execution risk

The bear case is not imaginary, and it deserves honest treatment.

Net debt of €1,113 million excluding lease liabilities is substantial. When lease liabilities are included under IFRS 16, total financial obligations stand at €3,048 million. The company has contracted to pay rent on 1,716 clubs for the next decade or more, and those obligations do not disappear if trading conditions deteriorate. A European recession, a prolonged inflation cycle that erodes consumer discretionary spending, or a competitive disruption to the low-cost gym model could all pressure membership retention. At €24.91 per month, Basic Fit is close to the bottom of the price range for any consumer subscription. It is not luxurious enough to be cut first, but it is not cheap enough to be entirely recession-proof.

The convertible bonds remain a medium-term cost-of-debt issue. The June 2026 put option has been waived via a €2.75 million fee, removing the near-term liquidity event. But the 2028 maturity still requires refinancing €304 million at current market rates, adding approximately €9 million in annual cash interest versus the current 1.5 percent coupon. That is a permanent headwind on FCF that investors need to account for in any forward earnings model. The company’s first quarter of 2026 will also be closely watched for signs of member retention in the post-January attrition window.

Germany remains an open question. Basic Fit’s owned presence in Germany is still nascent, with 44 clubs against hundreds in France. The Clever Fit franchise network provides market leadership by club count, but franchise revenue is a small fraction of owned club revenue. If the rebranding of Clever Fit clubs and the franchise management integration consumes management bandwidth, the core markets could suffer from distraction.

Retained earnings on the balance sheet stand at negative €317.7 million, reflecting years of heavy investment and the accounting impact of IFRS 16 lease costs. While this does not directly constrain operations, it limits dividend capacity and may create covenant sensitivity in certain lending agreements.

The valuation at roughly 9 times underlying EBITDA less rent looks cheap relative to peers, but it has been cheap for some time. Multiple expansion requires the market to believe in the franchise pivot story. If the Capital Markets Day on April 21 disappoints, or the 2028 bond refinancing signals a higher cost of debt than expected, the near-term catalyst fades and the stock drifts back toward the low end of the analyst range.

What to watch

The near-term playbook is clear. The first marker on the debt front is any communication around the longer-term capital structure, including early refinancing signals for the June 2028 bond maturity. With the June 2026 put option waived, the acute pressure is gone, but investors will want clarity on the likely cost of the 2028 refinancing and whether management plans to reduce gross borrowings ahead of that date via FCF generation.

The Capital Markets Day on April 21 is the strategic pivot moment. Investors will be listening for three things: quantified franchise revenue targets, an explicit free cash flow guidance number, and clarity on how many new clubs Basic Fit plans to open over the next three years. A credible FCF-focused strategy presentation could be a meaningful re-rating catalyst.

Membership growth in early 2026 is the operational check. The company added over 200,000 members in the first ten weeks of 2026. If the Q1 2026 results maintain that trajectory, the underlying demand story remains intact. Watch also for yield: if average revenue per member per month crosses €25.50 in 2026, the EBITDA upside is substantial.

Germany is the long-term prize. Clever Fit’s 377 franchise clubs in Germany give Basic Fit enormous optionality. If the franchise model performs as intended, generating stable royalties at 7 percent of revenue across hundreds of clubs, Germany transitions from a theoretical growth market into a genuine earnings contributor without requiring meaningful capital.

Finally, watch for any pre-announcement of a 2028 bond refinancing. Locking in a new facility early, at a known rate, would remove the last significant uncertainty in the capital structure and could serve as a quiet but meaningful re-rating catalyst for investors who have been discounting the stock on leverage concerns.

The verdict: Buy

Basic Fit is not a straightforward story, but the direction is clear.

The headline net profit of €14.3 million on €1.42 billion in revenue looks thin. The leverage profile is not light. The convertible bond still matures in 2028 and will be refinanced at a higher rate. Anyone reading only the GAAP income statement will see a company barely breaking even. That reading misses the point entirely.

The business underneath the accounting is generating €647 million in operating cash flow, earning 31 percent ROIC on its mature club base, and transitioning from a capital-intensive growth model to a capital-light franchise operation. The FCF swing from negative €88 million to positive €26 million in a single year is not an accounting quirk. It is the consequence of a deliberate strategic pivot that management telegraphed and then executed ahead of schedule.

The stock has already moved from €20 to €31, reflecting the initial recognition of the FCF inflection. That move does not make this expensive. At €31, Basic Fit trades at approximately 9.1 times 2025 underlying EBITDA less rent, a meaningful discount to European leisure infrastructure peers that trade in the 11 to 14 times range. The discount exists because of leverage and bond uncertainty. The June 2026 put has already been waived. As the 2028 maturity comes into focus and gets refinanced, the remaining compression rationale fades.

The base case at 10 times puts fair value at €36. A franchise model that delivers in Germany and adjacent markets, combined with yield improvement toward €26 per member per month, supports a path to €50 and beyond. The analyst consensus already sits at €34. The Capital Markets Day on April 21 is the first major opportunity for management to articulate the franchise vision with numbers. That is the catalyst.

The behavioural engine that powers this business does not need people to go to the gym. It needs them to keep meaning to. In Europe, where fitness penetration remains well below American levels, that is a structurally durable source of recurring revenue. At €24.91 per month, most members will not cancel today. They will cancel next month, when they have definitely made up their mind. Then they re-sign in January.

Rating: Buy. Base case €36 to €50. Primary catalyst: Capital Markets Day April 21, 2026. Bond put option already waived; 2028 refinancing is the remaining capital structure watch.

Illustrative only. Not investment advice. Always do your own research.

Sources: Basic-Fit Annual Report 2025, Basic-Fit Valuation Report (Qapital internal, January 2024), Yahoo Finance (BFIT.AS, March 2026), MarketScreener analyst consensus data.