5 Quality stocks trading below 15x PE

Finding exceptional businesses at reasonable prices

Most investors chase growth stories at 30x earnings. Meanwhile, five household names are generating 25%+ returns on equity and trading at single-digit to mid-teen multiples.

This valuation gap isn’t random, it’s behavioral mispricing at work.

This week's focus:

Companies with ROE >25% trading below 15x PE. That’s exceptional profitability at reasonable prices. With 10-year treasury yields at 4%, these quality businesses offer an average equity risk premium of 7.2% above risk-free rates, nearly double the historical equity premium of ~4%.

Screening methodology:

Using our quality growth framework, we identified businesses with sustainable competitive advantages, strong returns on equity, and temporary valuation discounts.

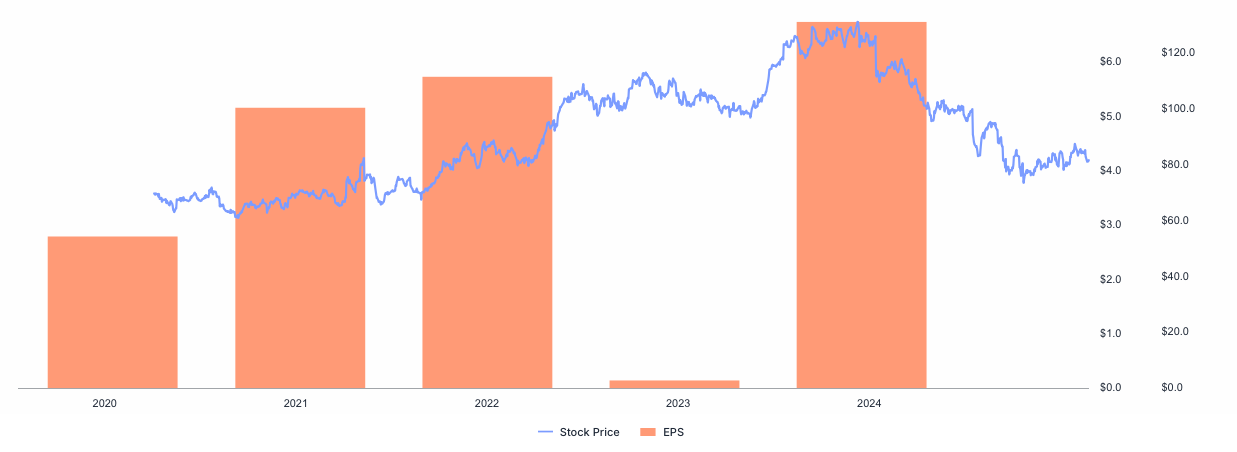

1. Merck & Co (MRK)

Market Cap: $218B | Country: US | Sector: Pharmaceuticals

Key Metrics:

• PE Ratio: 13.5x (vs pharma avg 16.2x)

• ROE: 28.2%

• Revenue Growth (1Y): Modest but stable

Why it's undervalued:

Markets obsess over Keytruda patent expiration while ignoring Merck's robust pipeline of cancer immunotherapies and their track record of successful drug launches. The company generates exceptional returns on invested capital and maintains pricing power in oncology.

Portfolio fit:

High - Defensive healthcare with pricing power and predictable cash flows

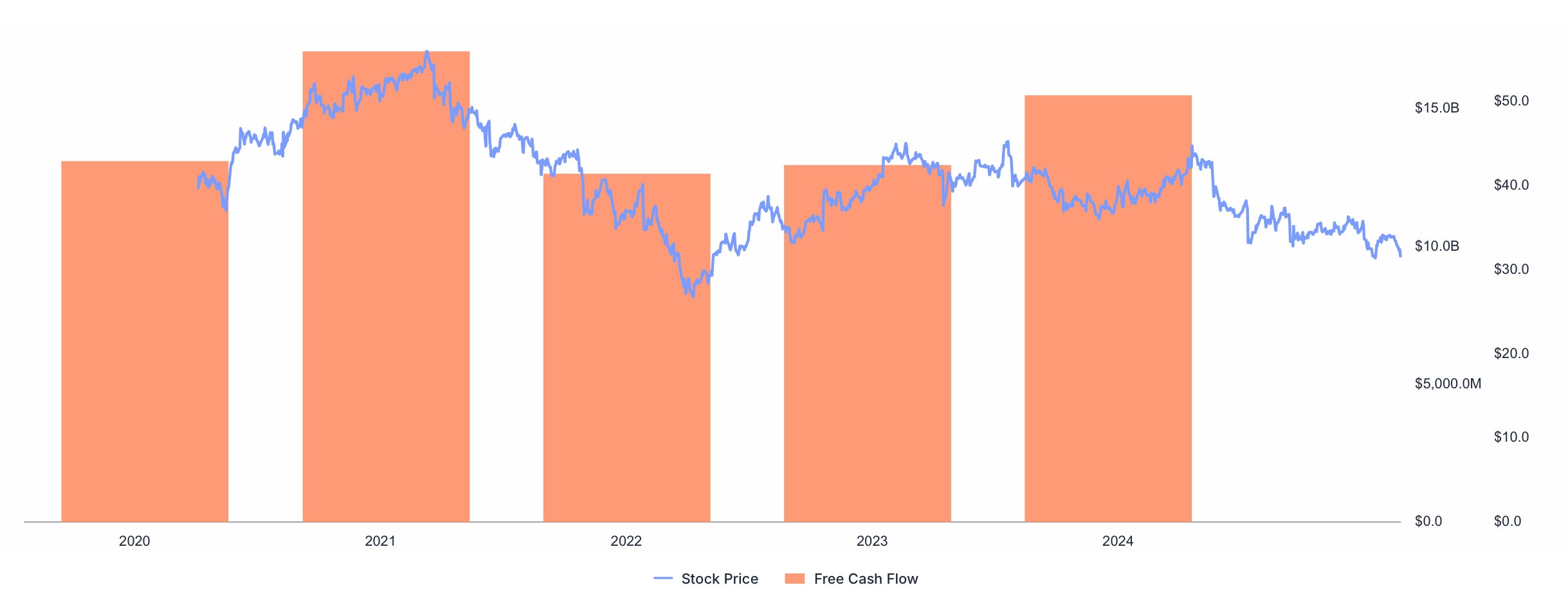

2. UPS (UPS)

Market Cap: $72B | Country: US | Sector: Logistics

Key Metrics:

• PE Ratio: 12.8x (vs logistics avg 18.4x)

• ROE: 34.9%

• Revenue Growth (1Y): E-commerce driven expansion

Why it's undervalued:

Concerns about Amazon's logistics expansion mask UPS's unmatched B2B network density and pricing discipline. The company's operational leverage creates substantial margin expansion during volume growth periods.

Portfolio fit:

High - Essential infrastructure with network effects and dividend income

3. Target Corporation (TGT)

Market Cap: $40B | Country: US | Sector: Consumer Retail

Key Metrics:

• PE Ratio: 10.4x (vs retail avg 15.8x)

• ROE: 26.3%

• Revenue Growth (1Y): Omnichannel strength driving consistent gains

Why it's undervalued:

Retail skepticism creates opportunity to own a differentiated brand with superior customer loyalty and omnichannel execution. Target's private label strategy and urban format expansion provide sustainable competitive advantages.

Portfolio fit:

Medium - Consumer discretionary exposure with operational excellence

4. Delta Air Lines (DAL)

Market Cap: $36.7B | Country: US | Sector: Airlines

Key Metrics:

• PE Ratio: 8.7x (vs airlines avg 12.3x)

• ROE: 28.5%

• Revenue Growth (1Y): Travel recovery driving strong performance

Why it's undervalued:

Cyclical bias obscures Delta's premium market positioning and operational discipline. The airline's hub dominance in key business markets and loyalty program create sustainable competitive moats in a commoditized industry.

Portfolio fit:

Medium - Cyclical exposure but best-in-class operator with fortress balance sheet

5. Comcast Corporation (CMCSA)

Market Cap: $117B | Country: US | Sector: Media & Telecom

Key Metrics:

• PE Ratio: 5.1x (vs media avg 14.7x)

• ROE: 25%

• Revenue Growth (1Y): Broadband strength offsetting cable headwinds

Why it's undervalued:

Cord-cutting fears ignore Comcast's broadband monopoly in key markets and the recurring revenue nature of internet services. Theme park recovery and streaming growth provide additional upside optionality.

Portfolio fit:

High - Infrastructure-like broadband business with content leverage and strong cash generation

Portfolio Construction Insight

These opportunities reflect a common behavioral pattern: markets temporarily misprice quality when faced with sector-specific concerns. Companies with strong competitive positions and disciplined capital allocation typically see valuations normalize as operational excellence becomes apparent.

For portfolio builders: These represent the type of opportunities that compound wealth over decades - quality businesses with pricing power temporarily available at reasonable prices due to short-term sentiment.

Risk consideration: Economic slowdown could pressure cyclical names like Delta and Target, while regulatory changes may impact pharmaceutical pricing for Merck.

Bottom Line

Quality companies with ROE >25% are trading at 35% discount to their 5-year average valuations, creating compelling entry points for patient capital focused on long-term wealth building.

Your next move: Review your portfolio’s quality exposure. If you’re overweight speculative growth and underweight cash-generating businesses with competitive moats, these five warrant deeper analysis.

Next week: We'll examine companies with FCF yields >6% and consistent revenue growth - cash generation machines trading below fair value.

Want the complete evaluation framework? Our QAPITAL methodology provides systematic analysis of quality, competitive advantages, and intrinsic value for portfolio builders. Subscribe to get access.